Fraud Article

Online shopping fraud prevention: A guide for marketplaces

This guide covers common ecommerce fraud threats like stolen cards, account takeovers, refund abuse, and AI attacks. It also outlines nine practical steps to strengthen your defenses. You’ll find actionable strategies to protect revenue, maintain customer experience, and stay ahead of risks, whether you have a dedicated fraud team or not.

Online shopping fraud prevention often brings to mind chargebacks, lost revenue, and damage to your brand’s reputation. For ecommerce teams, the natural response is to tighten security, consult with developers, or adjust payment provider settings. The challenge is stopping criminals while ensuring a seamless checkout experience for legitimate customers. A strong fraud prevention strategy is not just about security; it’s a vital part of the customer experience that protects your bottom line and builds trust.

This guide outlines the most common types of online shopping fraud, their warning signs, and nine practical security measures you can implement. We will also explore how the rise of AI-driven commerce is creating new challenges and what you can do to stay ahead. The focus is on actionable steps that don’t require a large, dedicated security team to put into practice.

Why fraud prevention is crucial for Ecommerce

Fraud directly impacts your revenue through bogus orders and chargebacks. It also erodes long-term brand trust when customers find unexpected charges or discover their accounts have been compromised. Beyond the immediate financial loss, fraud increases operational costs, raises payment processing fees, and complicates regulatory compliance.

Think of fraud prevention as you would your checkout user experience. If you don’t design it with intention, it will quietly cost you money every day. Prevention that is too visible creates friction and leads to lost sales. Prevention that is invisible to good customers results in higher acceptance rates and fewer losses.

Common fraud threats and their impact

Understanding the primary ways criminals attack online stores helps you build a more effective defense.

- Stolen card transactions: This is the most straightforward type of fraud. Criminals use stolen credit card information to make purchases. The result is an immediate financial loss for you, plus the cost and hassle of chargebacks when the real cardholder disputes the charge.

- Account Takeover (ATO): Attackers gain access to a customer’s account to place orders, steal loyalty points, or misuse saved payment methods. ATO attacks severely damage user trust when customers discover unauthorized activity linked to their profile.

- Friendly fraud: This occurs when a legitimate customer makes a purchase but then disputes the charge with their bank, claiming it was fraudulent. While not malicious in the same way as other fraud types, it creates significant administrative burdens and financial losses.

- Refund and return scams: Fraudsters exploit lenient return policies to get money or goods improperly. They might return stolen merchandise, an empty box, or a different, cheaper item to claim a refund.

Each of these attacks affects your business differently. Payment fraud hits your revenue directly, account takeovers damage customer loyalty, and return scams can deplete your inventory. Together, they create a compounding negative effect on your margins, operations, and brand.

Explore key fraud statistics, regulatory shifts, and actionable recommendations from Veriff’s new report.

The new frontier: AI-powered commerce and fraud

A significant shift is underway with the emergence of AI shopping agents. Powered by large language models, these tools can research products, compare prices, and even complete purchases without direct human involvement. This “agentic commerce” could disrupt traditional marketplaces by reducing the need for consumers to visit websites directly.

Platforms are already reacting. eBay has updated its terms to restrict autonomous purchasing bots, while Amazon has taken legal action against an AI company whose shopping agent accessed its platform. The core concern for merchants is losing control over the customer relationship, brand visibility, and valuable consumer data.

From a security perspective, AI agents introduce new fraud risks. When payment decisions are handled by external, automated systems, it can become more difficult to verify the legitimacy of a transaction. Retailers must decide how to engage with this new technology while protecting their data, customers, and revenue.

Key warning signs of weak defenses

Recognizing common warning signs allows you to spot security gaps before they lead to major losses.

- Suspicious order patterns: Be wary of multiple high-value orders from the same IP address or device, a sudden burst of orders from newly created accounts, or mismatches between shipping and billing addresses.

- Mismatched customer data: Look for inconsistent email domains, phone numbers that fail validation checks, or names that don’t align with payment details.

- Unusual login behavior: Monitor for repeated failed logins, access from unexpected geographic locations, or rapid switching between devices, as these can indicate an account takeover attempt.

Early detection reduces the burden on your operations and customer service teams. Every fraudulent order you block protects not just your revenue, but also your customers’ trust in your brand.

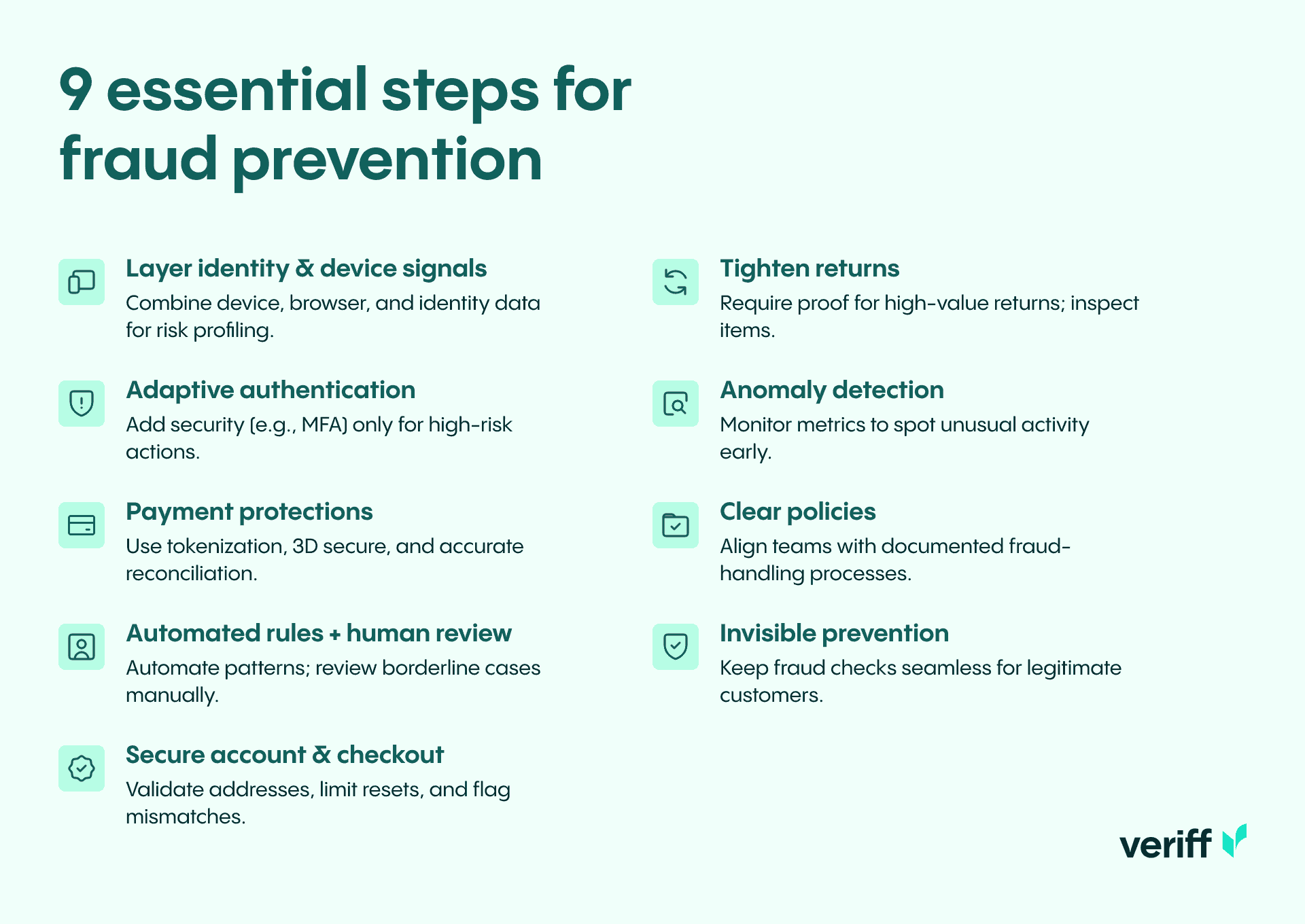

9 essential steps for fraud prevention

- Build layered identity and device signals

Collect and correlate various signals to make it more expensive and difficult for fraudsters to attack. Device fingerprinting, browser data, and network metadata provide early clues that help distinguish bots from real shoppers. Combine these with identity attributes like email age and phone number verification to create a comprehensive risk profile. - Use risk-based, adaptive authentication

Apply extra security measures only when the context warrants it. Risk-based authentication adds friction, like multi-factor authentication (MFA), selectively for logins or high-value checkouts that show elevated risk signals. This approach keeps the checkout process smooth for most customers while adding scrutiny where it’s needed most. - Implement strong payment protections

Leverage features from your payment provider, such as tokenization, to avoid storing raw card data. Enable 3D Secure (3DS) where it improves chargeback liability outcomes. Ensure your payment reconciliation processes are accurate so you can identify disputed transactions promptly. - Combine automated rules with human review

The most effective fraud strategy uses machines to catch patterns and people to understand context. Start with a conservative set of automated rules, such as blocking orders from anonymized proxies or limiting purchase velocity on new accounts. Flag borderline cases for a human review team to assess. - Harden account and checkout flows

Protect key points in the customer journey, including registration, password resets, and address changes. Require email verification for new accounts and rate-limit password reset attempts. At checkout, validate shipping and billing addresses and flag mismatches for review. These measures reduce account takeover risk. - Strengthen post-purchase and return controls

Refund and return fraud often succeeds due to lax policies. Tighten your return process by requiring proof of purchase or identity verification for high-value returns. Inspect returned items carefully and consider holding refunds for suspicious patterns while you investigate. - Monitor behavior with anomaly detection

Use analytics to spot emerging threats. Real-time monitoring of metrics like authorization decline rates, chargeback rates, and new account creation can provide early warnings. Correlate spikes in these metrics with marketing campaigns or site changes to rule out legitimate causes. - Define clear policies and empower your team

Create documented policies for handling order holds, cancellations, refunds, and chargebacks. Ensure that your fraud, customer service, and operations teams share the same playbooks and escalation paths. This cross-functional alignment leads to faster, more consistent decisions. - Design fraud prevention to be uinvisible

Your goal is to make your store the safest place to shop online without turning away good customers. Strong fraud prevention should feel invisible to legitimate buyers. You can achieve this by using progressive profiling, deferring non-essential checks until after a purchase, and communicating clearly when extra verification is required.

Conclusion: A continuous and balanced approach

Fraud prevention is not a one-time project; it’s an ongoing process. Attackers constantly adapt, so your defenses must evolve as well. Success lies in finding the right balance between security and customer experience.

By implementing layered security signals, adaptive authentication, strong payment protections, and disciplined internal processes, you can significantly lower fraud losses. This protects your revenue, preserves your brand’s reputation, and ensures customers continue to trust you. Leadership buy-in and a culture of continuous improvement are essential for maintaining an effective defense in the ever-changing world of ecommerce.