IDV Article

Cracking the code: Why localization is the key to identity verification success in APAC

APAC’s digital landscape is as diverse as its markets, with unique regulations, ID systems, and consumer habits. A global KYC flow that works in New York often stumbles in Jakarta, leading to false declines, compliance risks, and poor user experiences. In a region where onboarding delays cost banks clients and false declines rack up $443 billion globally, localization isn’t just important—it’s critical.

APAC is a mosaic of markets, each with its own regulatory frameworks, government ID systems, and consumer behaviors. From mobile-first habits to the prevalence of super apps, the region’s digital landscape is unlike any other. A global Know Your Customer (KYC) flow that works in London or New York will likely stumble in Jakarta or Mumbai. Why? Because it fails to account for local nuances like document types, languages, and trust signals.

This lack of localization can lead to three major risks:

- False declines – Lost revenue in price-sensitive markets where customer acquisition costs (CAC) are high.

- Compliance gaps – Regulatory penalties and barriers to long-term market access.

- Poor user experience – Frustrated customers who abandon onboarding, giving local competitors the edge.

The stakes are high. For example, nearly 90% of banks in Singapore report losing clients due to onboarding delays. Additionally, false declines globally are estimated to cost businesses $443 billion annually, a staggering figure that dwarfs the $6.4 billion lost to fraud. False declines—where legitimate transactions are mistakenly flagged as fraudulent, don’t just result in lost sales; they damage brand reputation and drive customers to competitors.

Regulatory complexity: A fragmented landscape

APAC’s regulatory environment is a patchwork quilt of KYC thresholds, anti-money laundering (AML) rules, and data protection laws. What’s compliant in one country might be a violation in another. For instance, data residency laws dictate where biometric data and ID images can be stored, while licensing requirements vary across industries.

Treating compliance as a mere checkbox is a recipe for delays and risks. Instead, businesses must design IDV workflows that are flexible enough to adapt to each market’s unique requirements.

The diversity of ID documents and data sources

Unlike Western markets that rely heavily on passports and driver’s licenses, APAC features a wide array of ID type, national ID cards, tax IDs, voter IDs, and even mobile ID schemes. Each comes with its own formats, languages, and security features. Some countries offer real-time government APIs for identity verification, while others require alternative methods.

To succeed, IDV systems must:

- Recognize local scripts and fonts.

- Extract structured data accurately.

- Validate unique security features.

Overlooking these details leads to manual reviews, higher decline rates, and frustrated users. In APAC, it’s not the technology that fails; it’s the lack of localization.

Language, UX, and mobile-first realities

APAC’s mobile-first culture adds another layer of complexity. With a wide range of Android devices, varying camera qualities, and inconsistent network speeds, IDV systems must be robust yet adaptable. Add to this the linguistic diversity, users expect interfaces in their local languages, complete with culturally relevant date formats and input patterns.

A seamless user experience means:

- Native language instructions and error messages.

- Optimized capture flows for low-light and low-bandwidth conditions.

- Integration with local payment and onboarding systems.

What works on a laptop in Sydney might fail on a budget smartphone in Manila. Localization isn’t just about translation. It’s about designing for real-world conditions.

Fraud patterns: Local problems need local solutions

Fraud in APAC doesn’t follow a global script. From synthetic identities to document fraud, the tactics vary by market. For instance, multi-SIM phones and shared devices are common in some regions, influencing fraud patterns.

Localized fraud models that incorporate regional trust signals, like mobile operator data or utility records, can significantly reduce false positives and improve approval rates. The result? Lower operational costs and a smoother user experience.

The identity landscape: A study in contrasts

APAC’s identity documents range from gold-standard security to high-risk vulnerabilities. Countries like Australia, New Zealand, Singapore, and Hong Kong issue some of the most secure credentials globally, often matching or exceeding North American standards. For example:

- Australian passports meet NIST “Superior ID” criteria with ICAO-compliant biometric chips, polycarbonate materials, and laser-engraved portraits, contributing to a document fraud rate of just 0.13%.

- Singapore’s identity card is a polycarbonate card with embedded chips and holograms, though it still faces fraud risks through digital manipulation.

In contrast, legacy, paper-based documents in countries like the Philippines and Indonesia present significant vulnerabilities:

- Philippine TIN cards lack chips, holograms, or MRZs and even require holders to glue on their own photos, contributing to a 10.15% fraud rate.

- Indonesia’s older ID cards are prone to data manipulation, though newer polycarbonate versions offer improved security.

Why localization drives revenue

Every abandoned verification is a lost customer. In APAC’s competitive, price-sensitive markets, a localized onboarding experience can be the difference between winning and losing customers. It’s not just about compliance, it’s about conversion.

Localized KYC flows:

- Turn abandoned verifications into active users.

- Reduce fraud-related losses.

- Lower compliance costs by aligning with local regulations.

In short, localization isn’t an operational tweak, it’s a growth strategy.

Practical guide to effective localization

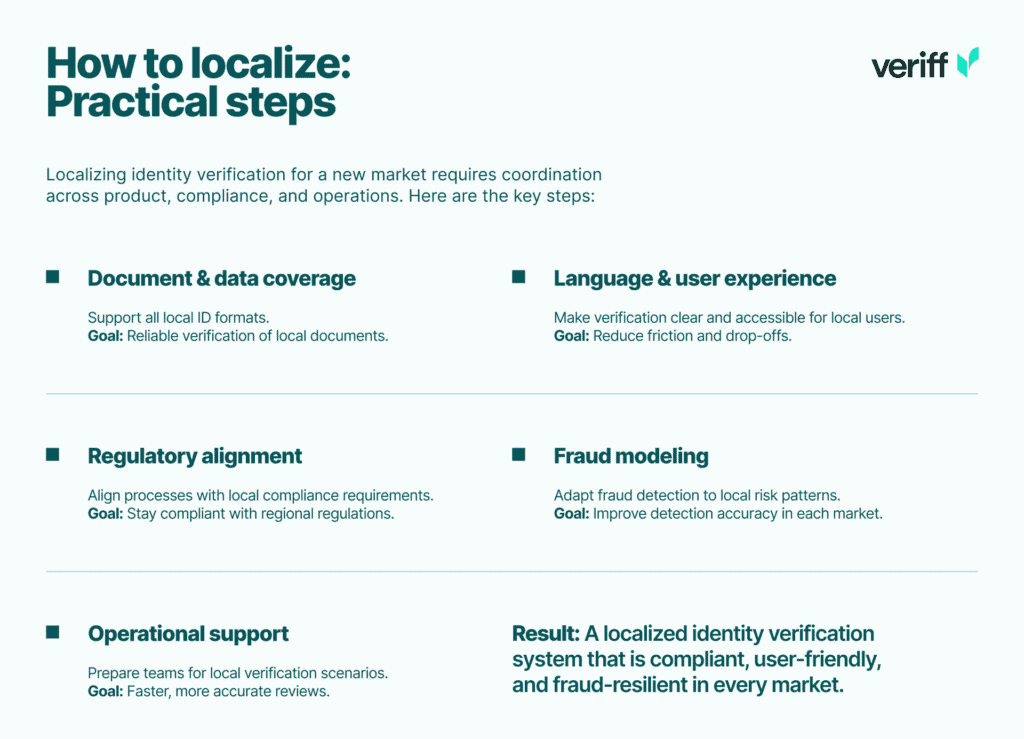

Localization requires a coordinated effort across product, compliance, and operations. Here’s how to get started:

- Document and data coverage – Support all local ID types and integrate with government or third-party APIs where available.

- Language and UX – Provide instructions in local languages and optimize for mobile devices.

- Regulatory alignment – Configure KYC workflows to meet local compliance requirements.

- Fraud modeling – Incorporate local trust signals and fraud patterns into risk scoring.

- Operational support – Train review teams on local documents and fraud behaviors to reduce latency.

Final thoughts

APAC’s diversity demands a localized approach to identity verification. By tailoring workflows to local regulations, documents, and user behaviors, businesses can unlock growth, reduce fraud, and build trust. In this region, localization isn’t just an enhancement—it’s the foundation for success.

Ready to expand into APAC with confidence?

Contact us for a personalized consultation or demo