Scaling with confidence: How fintech fraud prevention fuels growth

In fintech, fraud prevention is shifting from a compliance cost to a key driver of growth and trust. As fraud becomes more sophisticated, companies are re-evaluating the balance between security and customer experience. The future belongs to those who can stop fraud without hindering growth, using trust as a business asset, not just a regulatory requirement.

Introduction: the new role of fraud prevention in fintech

As digital finance matures, fraud prevention for fintechs is being recast from a cost center and compliance checkbox into a strategic growth enabler. Fintech executives increasingly recognize that safeguarding customers and minimizing risk directly supports customer trust, faster onboarding, and higher approval rates—outcomes that matter to top-line performance and market differentiation.

The costs are mounting. Veriff’s 2025 Future of Finance research revealed a 21% rise in fraud attempts year-on-year, with one in every twenty verification attempts involving someone pretending to be someone else. For some organizations, fraud has consumed as much as twenty percent of annual revenue, effectively becoming a hidden “fraud tax” on growth.

In Brazil, the situation is particularly alarming. Fraud attempts have surpassed one million per month in 2025, according to Serasa Experian, with scams ranging from deepfake-enabled impersonations to account takeovers. Kaarel Kotkas, founder and CEO of Veriff, emphasizes the importance of proactive measures: “Our mission is to ensure that real people have access to services, while criminals are stopped in a smart and scalable way, even in the face of increasingly sophisticated threats.”

In this environment, preventing identity fraud in fintech is not simply an exercise in risk management. It is an essential step in securing profitable growth, meeting regulatory obligations, and ensuring the business is positioned as a trusted leader in a crowded market. As Hubert Behaghel, Veriff’s Chief Product and Technology Officer, emphasized during the ID Talk podcast, “It’s about an infrastructure of trust. It’s not discrete capabilities that you plug specifically into different parts of the journey. You need to have this full ecosystem that empowers you to deal with the core of trust.”

This article explains how advanced fraud prevention for fintech, when embedded into product and growth planning, can help organizations scale securely and compete in the future of finance.

“Our mission is to ensure that real people have access to services, while criminals are stopped in a smart and scalable way, even in the face of increasingly sophisticated threats.”

Kaarel KotkasFounder & CEO Veriff

Growth from compliance to competitive advantage: Rethinking fraud strategies

Historically, fraud controls were designed to satisfy regulators and limit losses. Today, fintech fraud detection solutions are evolving into products that enable faster customer acquisition and reduced churn. When fraud prevention is treated as a strategic capability rather than a back-office function, it unlocks new revenue opportunities and lowers operating friction. Fintechs that treat fraud prevention as a product feature, not a back-office function, grow faster and churn less.

Several market studies and industry analyses show that companies prioritizing security and frictionless experiences tend to retain customers longer and achieve higher lifetime value, underscoring the commercial case for reframing fraud prevention as a growth lever, not merely a compliance requirement.

Building trust: Why security is foundational to customer loyalty

Trust has become a core product attribute for fintechs. Customers equate safe, reliable services with professional competence; conversely, accounts compromised by fraud erode confidence and lead to churn. “In fintech, trust is the product. Fraud prevention is how you protect it—and grow it.”

Evidence from consumer-trust research indicates trust influences financial product adoption and engagement. This is especially relevant in markets where consumers are rapidly transitioning to digital-first services. Fintechs that signal strong fraud prevention practices—transparent identity verification, fast resolution, and privacy-respecting analytics—are better positioned to win referrals and long-term relationships.

Moreover, regulators and partners increasingly interpret robust fraud controls as indicators of governance maturity. Demonstrating proactive fraud management reduces regulatory friction and can accelerate partnerships with banks, card networks, and payment processors—opening distribution and revenue channels that weaker peers may find inaccessible.

Data-driven defense: Leveraging technology for smarter fraud prevention

Data-driven fraud prevention is the engine that turns security into a business advantage. Machine learning fraud prevention in fintech, behavioral analytics, and real-time fraud monitoring for digital payments allows teams to detect sophisticated threats while minimizing false positives that block legitimate customers. The right combination of supervised learning models, anomaly detection, and adaptive workflows cuts manual review workloads and improves approval rates.

Fraud isn’t just a cost center—it’s a growth engine when it’s built to protect trust at scale. Technology powers that shift that balance precision with speed: ML models trained on device signals, transaction histories, and contextual risk factors; behavioral biometrics that distinguish bots from humans; and orchestration layers that apply policy in milliseconds to enable seamless onboarding.

Peer-reviewed surveys and industry reports have documented the effectiveness of machine learning in reducing detection latency and improving decisioning accuracy, while real-time monitoring platforms help teams intercept fraud at the moment it matters without introducing unnecessary friction for legitimate users.

Cross-functional collaboration: Aligning risk, product, and marketing

Strategic fraud management depends on organizational alignment. Risk teams hold domain expertise, product teams understand customer journeys, and marketing owns acquisition funnels—each group must collaborate to design fraud controls that protect trust without undermining growth. When these functions share metrics and co-own outcomes, fraud prevention becomes an enabler of product innovation rather than an obstacle to it.

Practical frameworks that support cross-functional collaboration include shared risk taxonomies, joint objectives (e.g., target net approval rates and acceptable false positive thresholds), and shared KPIs linking fraud outcomes to business metrics like conversion, retention, and unit economics. Embedding fraud signals into product experimentation pipelines allows teams to A/B test controls and measure trade-offs between protection and conversion in production.

The real competitive edge isn’t zero fraud—it’s zero friction for the right customers. That perspective drives tighter integration between fraud controls and customer experience, where policies are adaptive, and decisions are contextual rather than binary.

Future-proofing growth: Integrating fraud prevention into business planning

To secure sustainable, organic growth, fraud prevention must be part of strategic planning. That means budgeting for continuous model maintenance, investing in identity and data partnerships, and establishing cross-border policies that reflect local regulations and fraud patterns—especially important for fintechs operating across the US, the UK, Brazil, Mexico, and Colombia.

Operationalizing fraud prevention for long-term success involves several practical steps:

Treat fraud controls as product capabilities: define user-facing outcomes and measure their impact on acquisition and retention.

Invest in data infrastructure: ensure event streaming, privacy-compliant data enrichment, and secure storage to power machine learning and real-time decisioning.

Implement adaptive policies: set dynamic thresholds that respond to evolving threats while reducing false positives in benign scenarios.

Establish governance and post-incident learning loops: use fraud events as structured feedback to improve models, rules, and customer communications.

Strategic support and planning drive sustainable growth. Integrating fraud prevention into organic growth planning helps fintechs scale securely, adapt to evolving threats, and future-proof their business.

Strengthen your fraud prevention strategy for 2026

Explore key fraud statistics, regulatory shifts, and actionable recommendations from Veriff’s new report.

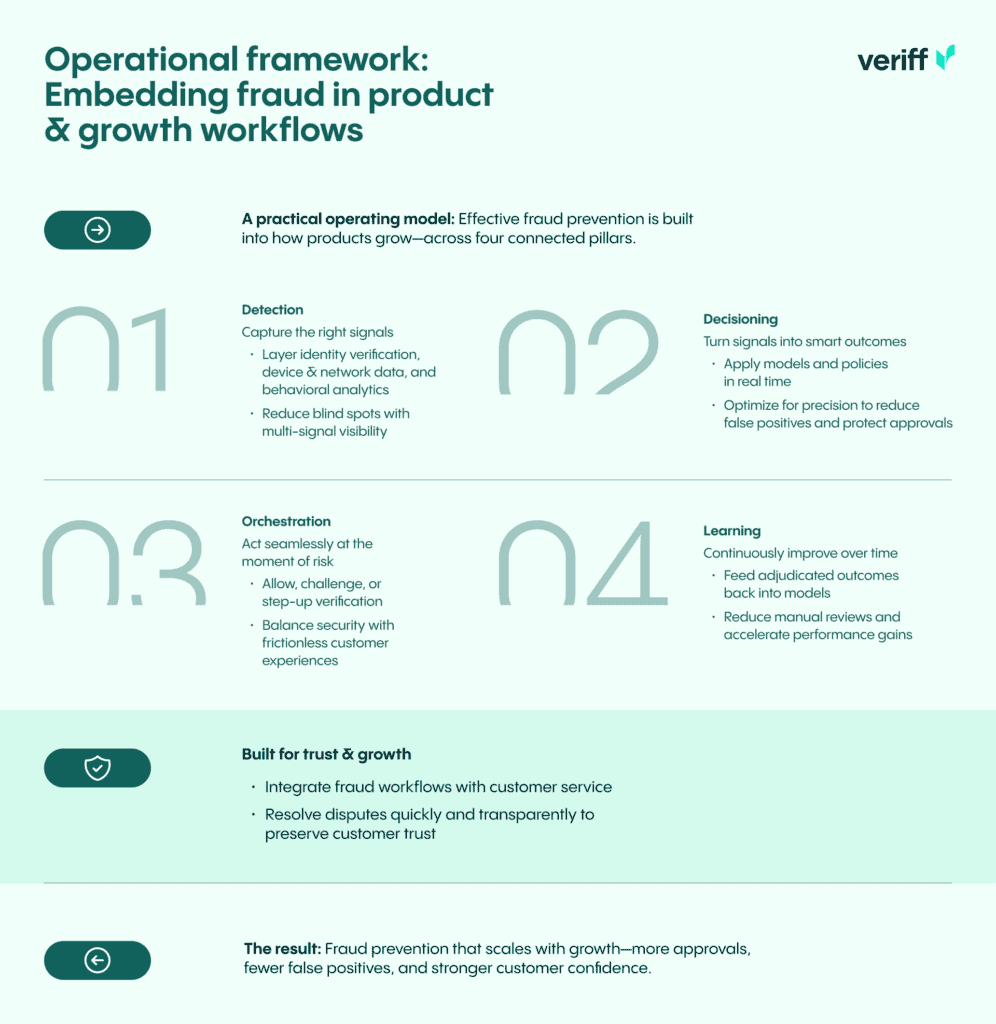

Operational framework: Embedding fraud in product and growth workflows

A practical operating model for embedding fraud prevention into growth includes four pillars: detection, decisioning, orchestration, and learning. Detection captures signals; decisioning applies models and policies; orchestration executes actions (allow, challenge, require additional verification); learning converts outcomes into improved models and rules.

Key implementation details:

Use layered detection: combine identity verification, device and network signals, and behavioral analytics to reduce blind spots.

Optimize for precision: tune models to minimize false positives while preserving detection of high-impact fraud—reducing false positives in fintech directly improves approval rates and customer satisfaction.[9]

Close the feedback loop: feed adjudicated outcomes back into training data to accelerate model improvement and reduce manual reviews over time.

Integrate with customer service: ensure dispute workflows and remediation are fast and customer-centric to preserve trust when incidents occur.

Metrics that matter: Connecting fraud KPIs to growth outcomes

Fintech leaders should track a balanced set of metrics that connect fraud performance to business outcomes. Core KPIs include net approval rate (approved minus fraudulent accounts), false positive rate, time-to-decision, manual review volume, customer dispute turnaround time, and fraud loss rate as a percentage of revenue. Linking these metrics to acquisition cost (CAC), cohort retention, and customer lifetime value (LTV) provides a clear view of how fraud prevention drives growth.

The most valuable asset on a fintech’s balance sheet isn’t capital—it’s customer confidence. Monitoring how fraud controls affect customer confidence and conversion enables leaders to make evidence-based trade-offs between protection and growth.

Regulatory alignment and cross-border considerations

Operating across the US, UK, Brazil, Mexico, and Colombia requires nuanced fraud strategies that respect local data protection and financial regulations. Harmonizing global policies with regional adaptations—while maintaining consistent customer experience—reduces regulatory risk and eases expansion. Proactive transparency with regulators and documented controls can also shorten time-to-market when entering new jurisdictions.

Realistic expectations and risk trade-offs

Leaders must accept that no system can reach zero fraud without creating intolerable friction. The strategic goal is to achieve the optimal trade-off: meaningfully reduce fraud while preserving or improving the experience for legitimate customers. “The real competitive edge isn’t zero fraud—it’s zero friction for the right customers.”

Practical governance requires leaders to define acceptable loss thresholds, backtest models regularly, and maintain contingency plans for emergent attack vectors.

Conclusion: Making fraud prevention a pillar of the future of finance

Fraud prevention for fintechs is no longer an operational burden to be tolerated—it’s a strategic capability that fuels sustainable growth, builds enduring customer trust, and creates competitive differentiation. By investing in advanced fraud prevention for fintech, leveraging machine learning fraud prevention in fintech contexts, and prioritizing real-time fraud monitoring for digital payments, fintechs can reduce false positives, accelerate onboarding, and confidently expand into new markets.

Fraud isn’t just a cost center—it’s a growth engine when it’s built to protect trust at scale.” When fraud prevention is designed as an integral part of product and growth planning, it transforms risk into revenue.

Ira BondarFraud Platform LeadVeriff

Call to action: Take the next step toward secure, sustainable growth

Ready to transform fraud prevention into a growth engine for your fintech? Connect with our experts today to benchmark your current strategy, discover actionable best practices, and unlock new opportunities as part of the future of finance. Contact us now to schedule a free consultation or download our comprehensive guide to building secure, scalable growth in fintech.

Take the next step

Stay ahead of fraud trends. Subscribe to our newsletter for the latest research, data, and industry insights.