Blog Post

Anti-money laundering guidelines — what are they?

What are anti money laundering guidelines, why are they important and what practices need to be followed? Learn more in our latest guide.

Anti-money laundering processes have never been more important for businesses dealing with finance.

In a world where money is increasingly digitized, and where there is a constantly expanding volume of data and devices for criminals to exploit, there are more and more opportunities for malicious financial activities to take place. At the same time, regulations are being strengthened around the world, and a greater ethical and moral responsibility to ensure that fraudulent or criminal transactions are cut off at the source.

But what does this mean from a practical perspective: for the banks, financial institutions, credit unions, insurers and real estate companies who have to comply with AML requirements. This blog explores the issue in detail.

What are anti-money laundering guidelines?

Anti-money laundering guidelines are sets of rules that certain businesses are expected to comply with, in order to ensure that illegal transactions can’t take place, and that those attempting them are reported to the authorities.

The guidelines vary from country to country. Generally, they set out the need for relevant businesses to verify the identity of an individual or business, check that their name, address and other key information is accurate and truthful, and investigate their financial activity to ensure that everything is above board. They also require prompt and detailed reporting of any irregular or potentially illegal activity, and these reporting requirements are getting stricter all the time. In the UK, for example, any discrepancies between the information they hold compared with that on the Companies House Register now has to be reported.

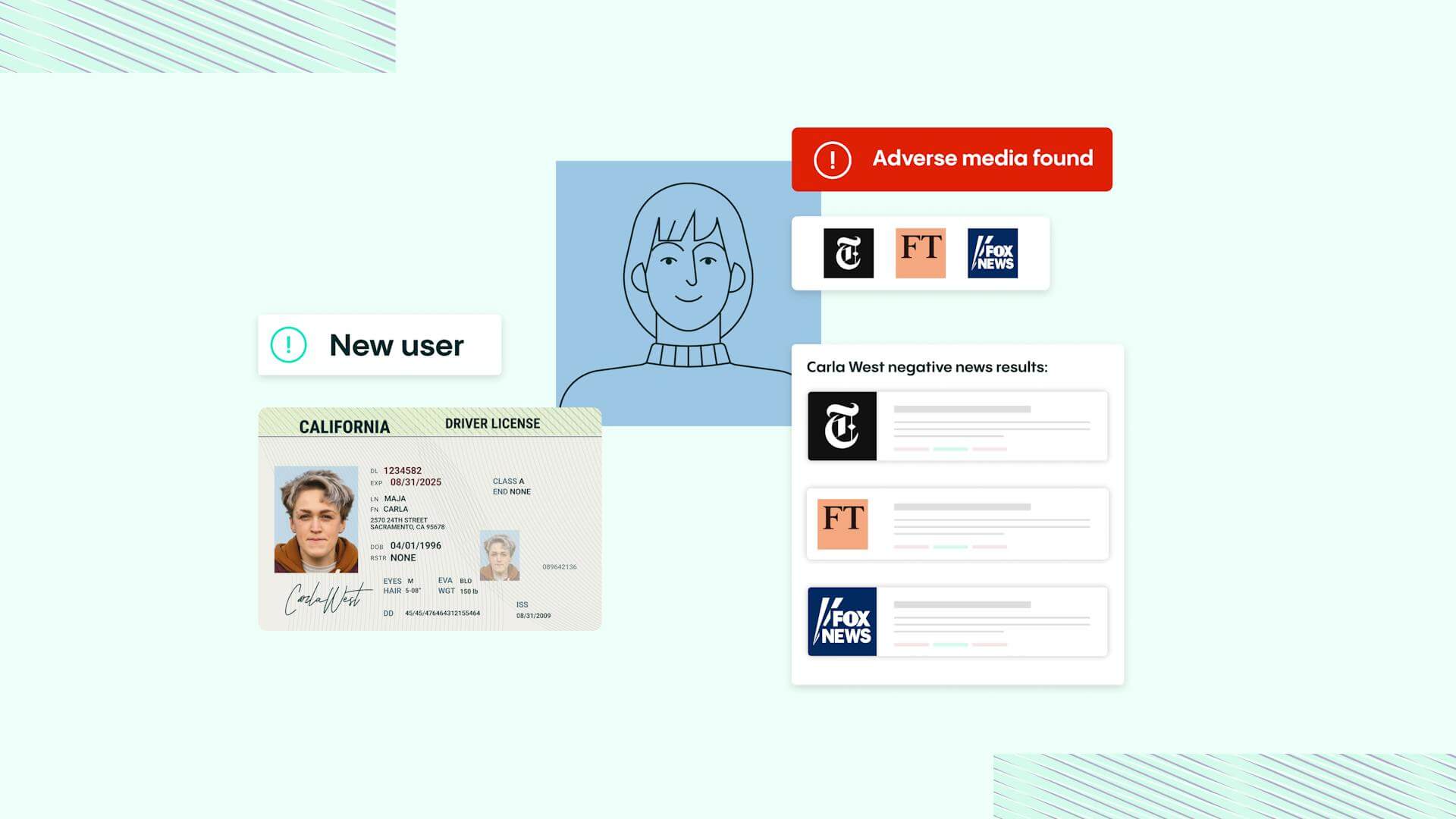

The main activity that relevant businesses have to undertake as part of AML procedures is commonly referred to as Know Your Customer (KYC), within which sits the Customer Due Diligence (CDD) process. These check identity, address (including business address if it’s an organization rather than an individual), financial records, and any other information that may indicate a high risk of impropriety. Strong CDD procedures will therefore include checks on government databases, in case certain individuals have criminal records, have sanctions against them, or if they are a Politically Exposed Person (PEP).

All of this information gives the financing business – and by extension, the authorities – a clear picture of the person or business making transactions, and how likely they are to attempt any fraudulent activity. Combined with ongoing monitoring which applies all of these checks on a constant basis, it means any money laundering activity should be stopped immediately, and in many cases, even prevented before an attempt can be made.

Relevant businesses are normally expected to comply with, and have their compliance supervised by, certain named regulatory bodies. As an example, in the United Kingdom, there are three main supervisory authorities: Her Majesty’s Revenue and Customs (HMRC), the Financial Conduct Authority (FCA) and the Gambling Commission. However, there are also a number of designated professional bodies who also have supervisory powers for businesses in their specific sector, such as the Law Society and the Institute of Chartered Accountants.

The importance of preventing money laundering can’t be overstated. Firstly, any financial institution found to have facilitated money laundering will be damaged severely, not only in the form of legal recourse by the authorities but also in terms of their public perception. But at a wider level, money laundering can be extremely damaging for society, because it gives the businesses carrying it out an unfair advantage over others. It can also reduce the tax take of a country, impacting the quality of public services that a government can provide to its people.

This is why there is such a strong responsibility, both legal and moral, on all finance-related businesses to stamp out money laundering wherever it may take place.

Types of guidelines for different sectors

Anti-money laundering guidelines vary between different types of business because the transactions involved can differ significantly. For example, banks have to safeguard against almost every type of transaction or money movement you can think of, while real estate companies have to be careful because of the large sums generally involved in buying property.

Here, we’ll explore some of the key characteristics of the anti-money laundering guidelines of four types of business:

Anti-money laundering guidelines for banks

For banks and other similar financial institutions, the main anti-money laundering requirements surround KYC processes. These should be carried out in accordance with the most up-to-date requirements, such as those with the European Union’s 5AMLD framework.

For example, when a customer attempts to open a new bank account, banks should collect information around their identity, and verify this information for accuracy. This can be done by verifying identity cards, using facial recognition technology, and in the case of businesses, checking invoices as proof of business address.

At a transactional level, banks should be able to screen payments and money transfers, in terms of the identities of both the sender and the recipient. Manual checks for this, however, are too slow, prone to human error and are simply impractical, given the huge volume of transactions that banks process every day. It’s therefore vital that technology is deployed that can automatically screen transactions against sender and recipient identities, and immediately highlight potential issues as soon as the transaction is attempted.

Anti-money laundering guidelines for insurers

Insurance providers, and life insurance providers in particular, are prone to money laundering attempts. This is because large amounts of money can flow in and out of policies at different times, and this is why there are stringent guidelines in place for insurers.

There are two main areas where compliance is expected from insurers. The first is in the monitoring of transactions, which apply to particular types of insurance policy: for example, the Bank Secrecy Act in the United States requires monitoring of permanent life insurance policies, some annuity contracts, and any product that includes investment functions or a cash value.

Any suspicious activity that is detected has to be reported to the authorities so that it can be investigated further; technology can help spot irregular actions, such as early surrender of a policy, using unusual payment methods, or borrowing large amounts soon after buying a policy.

The second area is enforcing financial sanctions in accordance with any applied by national and international governments. Insurers are expected to screen customers and check their identities against any sanctions lists that they may be on, either in the country of business, their country of residence or their country of origin. Customers should be screened on an ongoing basis, in case their status changes over time.

Anti-money laundering guidelines for credit unions

Credit unions may be less formal in their operations than a bank. But because of the nature of their lending activities, they have to be subject to the same kind of AML regulations as a bank, to ensure that they aren’t used by criminals as an easier option to sidestep controls.

As a result, credit unions must also conduct KYC checks in the same way banks do, incorporating Customer Due Diligence as well as Customer Identification Programs (CIPs). Additionally, many countries mandate reporting of all transactions made over a certain value: in the United States, this value is $10,000.

Credit unions don’t necessarily have the in-house resources to create and maintain sufficiently robust AML controls. This is where technology can make a big difference, saving time and human resource in automating many of the checks and applying regular monitoring. Additionally, some countries (such as the United States) allow different credit unions to share AML resources and information, so that they can co-operate and potentially fill each other’s gaps in compliance.

Anti-money laundering guidelines for real estate professionals

The use of property as a way to launder money and hold value within an asset has increased in popularity in recent years, in no small part to increases in the value of real estate in many developed and developing countries. It’s also worth noting that the large amounts of money involved in property purchases means that the sector naturally attracts the interest of many high net worth individuals, some of whom may not have acquired their wealth through legitimate means.

Real estate organizations are required to conduct customer due diligence on whoever the ultimate beneficial owner of a property is. As well as their financial wherewithal and their identity, real estate firms also need to cross-check their identities against sanction and PEP lists, to ensure they aren’t laundering funds from one state by buying property in another.

There are robust regulations over how any potential issues are reported to the relevant authorities, including any suspicious transactions. These should be reported quickly, so that authorities can take swift and decisive action to prevent crime, or to use the information as part of larger-scale investigations.

Areas of compliance to review

With the nature of financial crime evolving all the time, and regulations around the world being adjusted at a similar pace, complying with AML requirements is a constantly moving target. It’s therefore vital that all companies required to meet anti-money laundering guidelines regularly review their processes to ensure they continue to comply.

What this review consists of will vary depending on the sector a company is involved in, and the country (or countries) where they operate. However, there are several basic questions that should always be asked, such as:

- Are the right internal procedures in place to meet all regulations and compliance requirements?

- Are records of AML processing stored securely, and easily accessible if proving compliance is needed?

- Does a risk assessment consider the customer base of the company and the types of transactions and services involved?

- Are the right systems in place to ensure that information collected in customer due diligence and KYC is verifiably authentic?

- Does the CDD system include automated integration of cross-referencing against sanctions, criminal records and PEP lists in all relevant countries?

- How easily and quickly can suspicious activity and/or irregular transactions be reported?

- Do all staff involved in ensuring AML compliance have the required and up-to-date skills for processing, including effective use of any technology solution deployed?

AML best practices

As this blog ably demonstrates, there are lots to consider when ensuring a business is meeting its obligations around anti-money laundering guidelines. As well as exploring the above questions in any compliance review, these three strategies are vital to maintaining robust AML policies, both now and in the future:

- Constant monitoring: a person or business who may be compliant with AML regulations today may not remain so tomorrow, and activity that may seem above board may soon turn out to be criminal or fraudulent. That’s why KYC and CDD processing should be continuous, so that any changes in behavior that highlight a potential risk can be flagged to the authorities immediately.

- Regular regulatory reviews: just as customer activity changes over time, so can the regulations put in place by governments and authorities all over the world. All companies should review the rules on a regular basis in all the countries that they operate, to ensure that they don’t fall foul of changes, and so they can plan ahead for adjustments that have been scheduled for future introduction.

- Adopt technology and automation: AML compliance is necessary, but it’s also complex and potentially time-consuming. At the same time, criminals have become ever more sophisticated in forging identities, and the documents that they use to prove them. Using a technology solution, equipped with automation and machine learning, can help ensure that identity checks are conducted with much higher levels of rigor and accuracy than even a skilled and experienced human could hope to manage.

If you’re looking for a technology partner that can help you run comprehensive AML checks, then Veriff’s expertise and innovation are ideal. To find out more, book a consultation with Veriff.