Blog Post

What is Anti-Money Laundering?

Anti-Money Laundering, or AML, regulations exist to protect consumers all over the globe from fraud and financial crime. But what do the regulations entail, who do they apply to, and what are the crucial things to know?

Anti-money laundering, or AML, is the process undertaken by financial organizations to ensure they adhere to legal requirements in preventing, monitoring, and reporting illegal activity.

These regulations exist to protect consumers all over the globe from fraud and financial crime. But what do the regulations entail, who do they apply to, and what are the crucial things to know?

AML refers to the set of laws, policies, and regulations that financial institutions and companies in specific other fields have to apply to actively monitor clients and prevent financial crimes. It includes a wide range of activities, from corruption to manipulating the market. These measures help companies prevent fraudulent cases and avoid any kind of misunderstanding with their customers.

Most financial transactions need to comply with AML laws, especially when a customer is opening an account and starting to use a specific financial service.

In this article, we’ll try to tell you more about anti-money laundering in general and dive deep into this topic to discuss the major differences between AML and Know Your Customer regulations (KYC), compliance, laws, and verification.

What’s the difference between AML & KYC?

While AML refers to anti-money laundering, KYC stands for ‘Know Your Customer’, and relates to risk assessment and verifying identity. KYC is one part of the process that falls under the overall AML umbrella and contributes to the prevention of money laundering.

We can better understand the key differences between these terms by breaking them down into different components, such as process, purpose, elements, and features.

The AML process aims to implement specific regulations to prevent suspicious financial activities. The core elements of an AML framework are risk assessments of clients, risk management systems, KYC (or customer due diligence) programs, and relevant reporting obligations. These are to be implemented as an AML compliance program. The system should be comprehensive, detailed, and well-planned.

On the other hand, KYC is an obligation aimed at verifying clients, assessing risks, and gathering information about the clients. The purpose, in this case, is to make sure that suspicious clients or individuals do not gain an opportunity to launder illegal money. The core elements for KYC can be data collection, identity verification, risk assessment, politically exposed persons and sanctions screening, and subsequent management. The system should be thorough, credible, smart, and efficient.

To a layman, it might be easy to confuse AML and KYC. However, KYC is just a step that companies take in the broader AML framework, using KYC software as a reliable tool to detect fraud alongside customer verification.

What is AML compliance?

Financial institutions must adhere to an AML compliance program, which outlines what they must do to detect suspicious transactions, terrorist activities, and other financial crimes.

Companies at risk of financial crime are required to implement an anti-money laundering compliance program to avoid risks and do their job in the safest way possible. This program combines everything that the company is doing to meet the compliance norms: user-processing policies, reporting of money laundering incidents, built-in internal operations, and monitoring accounts. The main goal is to detect, respond, and avoid money laundering and fraud-related risks.

Businesses need to follow specific requirements to develop a robust AML compliance program. They can achieve this goal successfully if they take into account the following:

- Reporting effectively – It can be essential in different cases to immediately deliver information regarding money laundering activity to the relevant authorities.

- Being aware of the risk level of your customers – Businesses have to evaluate the risk profiles and make appropriate conclusions to process them accordingly, applying various measures.

- Having a compliance officer as a team member – These processes are not easy to manage and require a specific skill set to keep the business in step with ever-changing anti-money laundering regulations and laws.

The business representatives should keep in mind that compliance must be the moral responsibility of each employee within the company, across all organizational structures.

Several factors can impact AML compliance. The key factors are local and regional laws, including applicable guidance and recommendations. Business owners should understand current legislative requirements and keep an eye on future developments. This, and ensuring staff receive the correct training, can help level up the development of AML compliance procedures.

AML programs

A set of procedures that are designed to guard against a person using the company to facilitate money laundering is called an anti-money laundering program. There are several steps to take to develop a proper AML program, which can be effective for the company in the long run. The key components are:

- Detecting suspicious activities – The company should handle and quickly expose activities related to money laundering, such as finding fake data or abnormally big sums of money deposited into a particular account.

- Risk assessment – Different assessment models can help you effectively sort customers into threat tiers on your particular risk evaluation.

- Internal practices – It is crucial to develop and implement internal guidelines for companies regarding information sharing within the organization. You should make due diligence your focus point, assign roles, and report suspicious activities.

- Prevention of criminal attempts – Companies should carry out AML training programs regularly. Especially in departments where staff come into direct contact with clients, as improved knowledge gives them the insight to be more prepared for any situation, and spot suspicious signs.

- Independent audits – Finally, conducting a review with an independent auditor can be a fantastic way to spot the weaknesses in the company’s risk assessment and compliance. Companies can easily evaluate the effectiveness of their AML program and act if something needs to be fixed by reviewing audit reports.

What is the anti-money laundering act?

A legislative act concerning anti-money laundering related obligations in a certain jurisdiction is usually called the Anti-Money Laundering Act (although local laws might have different names, and anti-money laundering obligations can be covered in a legislative act with a different name).

The primary purpose of this act, and related regulations connected to it, is to combat money laundering and similar activities. Every entity that is subject to the framework has a responsibility to apply anti-money laundering-related obligations. However, the extent of the obligations might depend on the field of activity of that specific entity.

Countries and regional actors, like the European Union, update their frameworks from time to time to stay ahead of the curve and react to changes in the market.

Who enforces anti-money laundering laws?

The authority for enforcing AML laws can change from country to country. For example, in the United States, the AML framework for financial institutions is provided by the Bank Secrecy Act and its implementing regulations. This gives the Treasury Department (acting through the Financial Crimes Enforcement Network aka FinCEN) the power to enforce AML obligations coming from the Bank Secrecy Act.

In the UK, on the other hand, the Financial Conduct Authority is the main financial services regulator with authority over banks, credit unions, and other financial institutions. The Financial Conduct Authority works closely with the National Crimes Agency, overseeing compliance with AML regulations in the region and has the power to investigate money laundering cases.

AML identity verification

A good starting point for AML compliance in the digital world is online identity verification. KYC works with the main aim of identifying and verifying customers before letting them use your services. This should ideally be both convenient and understandable for the customer.

Verification, in general, is the process of ensuring that individuals, who try to access your service, are who they claim to be. Usually, identity verification takes place when customers are being onboarded to a service and before they can have access to it.

Identity verification is generally mandatory for all entities which are obliged under the AML framework. As mentioned, local legislation, together with rules and regulations enacted and enforced by government agencies, require entities to follow a set of procedures to ensure AML compliance. Generally, approved KYC procedures can include ID verification, checking information against separate and reliable sources, such as database comparisons and background checks.

What are AML checks?

Although applying KYC is an important step in AML compliance, AML-obligated companies need to run additional AML checks when they welcome a new client, and throughout the client’s lifecycle. Under the regulations, there is a legal obligation for companies to take steps to discover money laundering cases and report them properly.

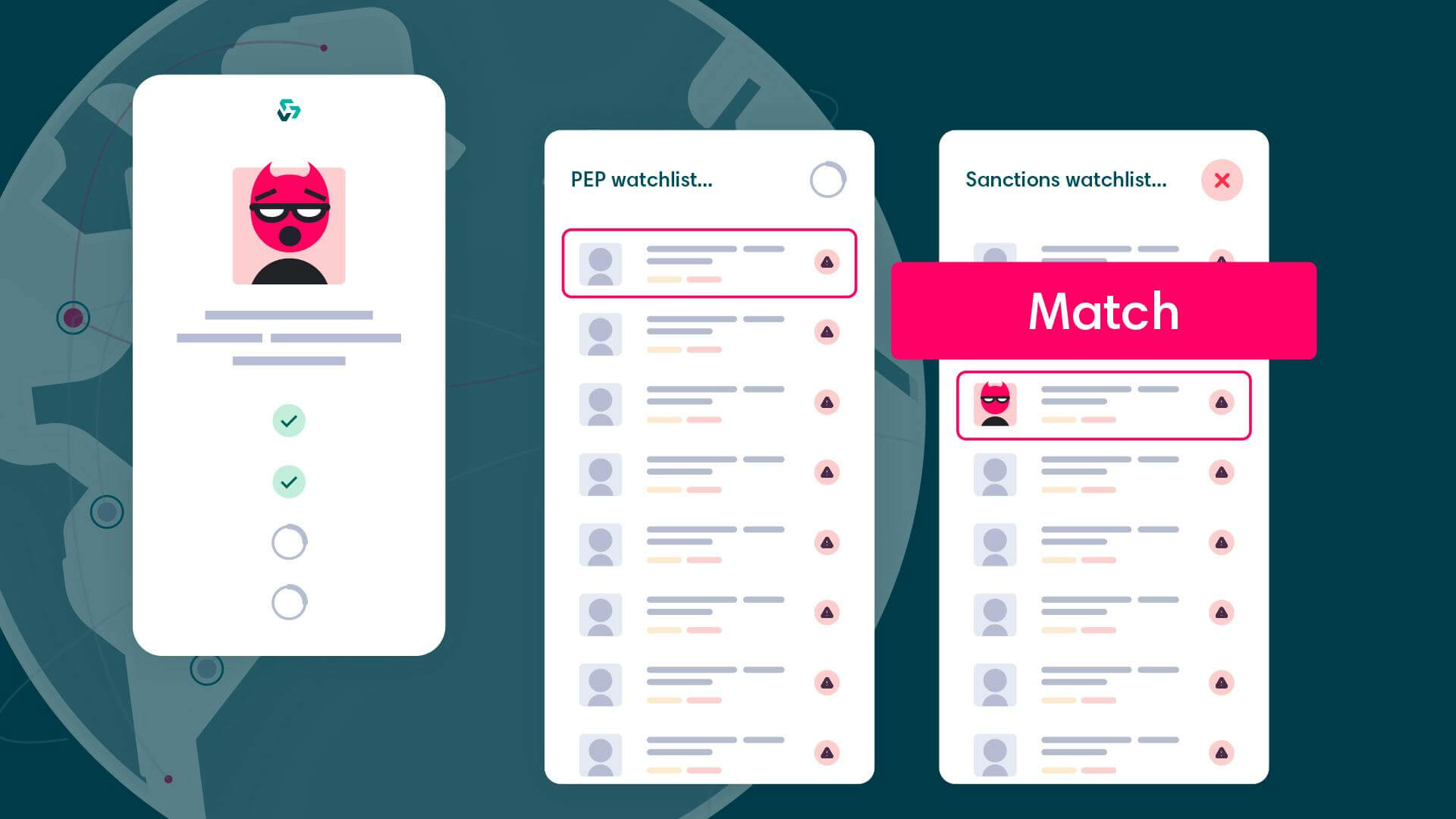

Companies should discover which clients are politically exposed persons and which potential clients could be under sanctions. Additionally, companies should actively monitor their customers’ behavior to detect suspicious and criminal activity in case it happens. We can summarize the foregoing as Anti-Money Laundering checks.

AML checks can differ depending on the laws applicable. As countries update laws frequently, companies should adapt to these fast. There are a few examples where companies and individuals have faced serious fines for non-compliance.

Ensure your organization is AML compliant

Here at Veriff, we work hard to build trust online and make the digital world safer with the tools we’re building daily. Take a look at our AML & KYC Compliance Solution, which can help your team fight against money laundering and other financial crimes.

Want to hear more about how you can do more to fight financial crime? Book a demo with a member of our team today.