KYC Article

APAC compliance made simple: Your trusted 2026 e-KYC guide

Navigating APAC’s financial regulatory landscape is becoming increasingly complex. With fragmented rules, rising AI-driven fraud, and stricter enforcement across markets like New Zealand, compliance teams face growing pressure to get onboarding right. This guide breaks down e-KYC, AML, and CFT requirements across five key APAC markets and shows how to build a scalable, future-ready onboarding framework for 2026 and beyond.

Navigating the financial regulatory landscape in the Asia-Pacific (APAC) region is increasingly complex making APAC compliance a growing priority for financial institutions operating across multiple jurisdictions. In New Zealand, a multi-regulator model splits compliance responsibilities: the Financial Markets Authority (FMA) oversees market conduct, the Department of Internal Affairs (DIA) supervises AML/CFT for payment and digital services, and the Reserve Bank (RBNZ) manages financial stability and prudential regulation for banks and insurers.

As digital banking and cross-border payments continue to accelerate across APAC, financial institutions are operating in an increasingly fragmented compliance environment. Each jurisdiction applies its own rules, enforcement priorities, and digital identity frameworks, making it difficult to design a single, consistent approach to customer onboarding.

For compliance teams, staying current is a full-time job. Financial crime, including increasingly sophisticated AI-driven identity fraud, is on the rise, and regulators across the region are responding with tighter supervision, stricter enforcement, and higher expectations around identity verification, ongoing due diligence, and risk monitoring.

This guide provides a clear, structured breakdown of APAC e-KYC, AML, and CFT requirements across five key markets. It highlights key regulatory trends and explains how financial institutions can build a scalable, future-proof onboarding framework designed to meet compliance demands in 2026 and beyond.

The importance of fast, risk-based onboarding in APAC

Getting onboarding right in the APAC region is not just about following rules; it’s about managing risk and protecting your institution’s reputation. AML and CFT enforcement actions are increasing, with significant penalties for non-compliance. A single failure can lead to significant fines and lasting reputational damage.

Regulators expect financial institutions to adopt a risk-based approach. This means your compliance framework must be able to identify, assess, and mitigate risks effectively. For compliance teams already stretched thin, the pressure to implement robust, efficient, and auditable systems is immense. Fast, compliant, and secure onboarding is no longer a luxury—it’s a fundamental requirement for survival and growth.

Country-by-country e-KYC & compliance breakdown

The core challenge of compliance lies in its diversity. Each country has unique requirements for electronic Know Your Customer (e-KYC) and digital identity verification. Here is a high-level overview of the rules for financial institutions in five key APAC markets.

Australia

Australian compliance is governed by the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act) and its associated Rules. The primary regulator, AUSTRAC, provides clear guidance on customer identification and verification.

- Primary regulators: Australian Transaction Reports and Analysis Centre (AUSTRAC)

- Key e-KYC rules: Financial institutions must perform applicable customer identification procedures (ACIP) before providing any designated service. This involves collecting and verifying customer information to be reasonably satisfied the customer is who they claim to be. The framework supports the use of electronic data and systems for verification.

- Risk-based requirements: The AML/CTF Act mandates a risk-based approach. High-risk customers require enhanced customer due diligence (ECDD), while ongoing monitoring is necessary for all business relationships.

New Zealand

New Zealand’s compliance framework is built on the Anti-Money Laundering and Countering Financing of Terrorism Act 2009. The Department of Internal Affairs (DIA) oversees its implementation, with specific guidelines for electronic identity verification.

- Primary regulators: Financial Markets Authority (FMA), Department of Internal Affairs (DIA), Reserve Bank of New Zealand (RBNZ)

- Key e-KYC rules: The Amended Identity Verification Code of Practice 2013 permits electronic verification using reliable and independent sources. This includes using government-backed digital identity services like RealMe.

- Risk-based requirements: The framework requires firms to have robust systems for conducting customer due diligence based on risk. Triggers for enhanced due diligence include complex transactions, high-risk jurisdictions, and politically exposed persons (PEPs).

Singapore

Singapore stands out as one of APAC’s most advanced and sophisticated compliance hubs. The Monetary Authority of Singapore (MAS) sets a high bar for technology adoption and risk management in the financial sector.

- Primary regulators: Monetary Authority of Singapore (MAS)

- Key e-KYC rules: MAS Notice 626 on Prevention of Money Laundering and Countering the Financing of Terrorism outlines detailed requirements for banks with MAS having a wide range of segment-specific issuances for other types of providers.

- Risk-based requirements: MAS mandates a rigorous, risk-based approach. The Financial Services and Markets Act 2022 and various circulars, like AMLD 01/2022, emphasize the need for ongoing monitoring and robust controls.

Malaysia

Malaysia is rapidly expanding its digital economy, and its regulatory framework is evolving to keep pace. Bank Negara Malaysia (BNM) has established a clear policy for e-KYC to support secure digital financial services.

- Primary regulators: Bank Negara Malaysia (BNM)

- Key e-KYC rules: The e-KYC Policy Document specifies requirements for customer onboarding using digital channels. It includes mandatory liveness detection and the use of approved biometric methods to ensure the customer is physically present during verification.

- Risk-based requirements: The Anti-Money Laundering, Anti-Terrorism Financing and Proceeds of Unlawful Activities Act 2001 (AMLA) forms the foundation of Malaysia’s AML/CFT framework. Financial institutions must implement risk-based controls and conduct due diligence as outlined in BNM’s policy documents.

Philippines

The Philippines has made significant strides in digital finance, driven by a need for greater financial inclusion. The Bangko Sentral ng Pilipinas (BSP) has updated its regulations to facilitate secure remote onboarding.

- Primary regulators: Bangko Sentral ng Pilipinas (BSP), Anti-Money Laundering Council (AMLC)

- Key e-KYC rules: BSP Circulars 950 and 1122 provide guidelines for e-KYC. The rules permit remote onboarding but require mandatory liveness detection to prevent fraud. The national digital ID, PhilSys, is being integrated to streamline verification processes.

- Risk-based requirements: Based on Republic Act No. 9160 (the Anti-Money Laundering Act), financial institutions must implement a risk-based customer identification and verification process. The focus is on preventing money laundering and terrorism financing through robust due diligence.

Regional trends shaping APAC compliance

Several macro trends are influencing the direction of compliance across the APAC region:

- Rise of government digital IDs: National digital identity systems (Singpass, MyKad, PhilSys) are becoming central to e-KYC processes, enabling faster, more secure, and more reliable customer verification.

- Mandatory biometrics and liveness: Regulators are increasingly mandating the use of biometric verification and liveness detection to combat identity fraud and ensure the integrity of remote onboarding.

- Tougher controls and penalties: Financial crime enforcement is intensifying, leading to stronger controls, higher penalties, and a greater emphasis on mitigating reputational risk.

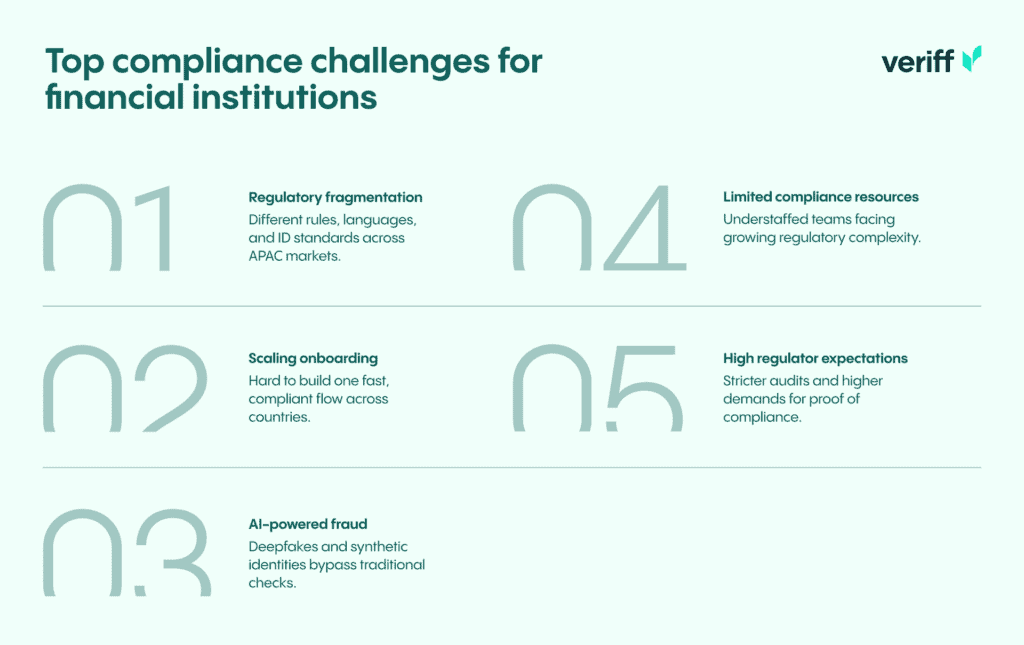

Top compliance challenges for financial institutions

Operating in APAC presents several distinct challenges:

- Regulatory fragmentation: Managing different rules, languages, and identity documents across dozens of markets is complex and costly.

- Scaling onboarding: Creating a unified, efficient, and compliant onboarding flow that works across multiple countries is a major operational hurdle.

- AI-powered fraud: Criminals are using deepfakes, synthetic identities, and other AI-driven tools to bypass traditional security measures.

- Limited compliance resources: Compliance teams are often understaffed and overwhelmed by the volume and complexity of regulatory demands.

- High regulator expectations: The expectation for perfect audit trails and demonstrable compliance has never been higher.

How Veriff helps financial institutions

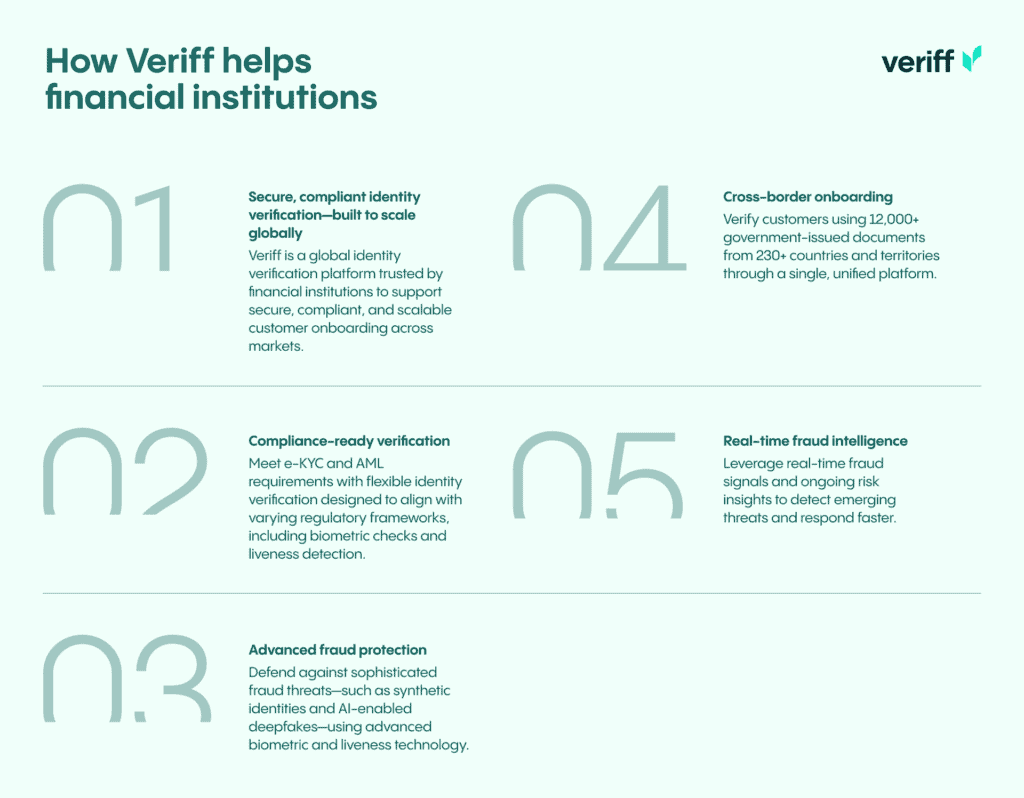

Veriff is a global identity verification platform trusted by financial institutions worldwide to support secure and compliant customer onboarding. Our AI-powered solution helps organizations build onboarding processes that scale internationally, while maintaining strong security and compliance standards. Veriff provides a comprehensive solution for identity verification, combining compliance-ready features with advanced fraud protection. We support customers in meeting their e-KYC and AML obligations through flexible verification capabilities, including biometric checks and liveness detection, which can be tailored to various regulatory requirements. Our advanced technology also helps defend against sophisticated fraud attempts, like synthetic identities and AI-enabled threats such as deepfakes. With Veriff, you can seamlessly onboard customers from around the world by verifying over 12,000 government-issued IDs from more than 230 countries and territories on a single platform. Additionally, our system provides real-time fraud intelligence and ongoing risk insights, enabling institutions to detect and respond quickly to emerging threats.

Conclusion

The APAC compliance landscape is defined by rapid evolution and significant complexity. For financial institutions, success depends on the ability to navigate fragmented regulations, combat advanced fraud, and manage reputational risk effectively.

Adopting a robust, risk-based approach is essential. With powerful tools like Veriff, you can automate identity verification, streamline cross-border onboarding, and stay ahead of financial crime. This frees your compliance team to focus on strategic risk management, ensuring your institution remains secure, compliant, and competitive in the dynamic APAC market.