Blog Post

Four easy steps to creating a frictionless AML process

Creating an anti-money laundering (AML) process is about striking the best possible balance between minimizing financial and reputation risk while avoiding unnecessary loss of business.

From financial services firms to real estate businesses, there are a range of sectors that are targeted by bad actors to launder money. In the fight against money laundering, money launderers and terrorists, anti-money laundering regulations have been established by law enforcement agencies to ensure that businesses can prevent the risk of crime and keep their customers safe. AML regulations take a number of forms, from the creation of suspicious activity reports to assessing politically exposed persons, with businesses expected to take a risk based approach in order to remain compliant. As such, businesses much ensure that their anti money laundering program is effective, up-to-date and user friendly.

As a growing business, you want to prioritise user experience and minimize friction in the onboarding process. But at the same time, you need to comply with regulations, as well as protect your business from reputational damage and financial crime.

For neobanks, money laundering is a serious potential issue. International standards set by the Financial Action Task Force (FATF) set out a clear framework of recommended preventative measures financial institutions should follow. These include requirements not only for customer due diligence to address potential money laundering, but also for additional measures regarding politically exposed persons (PEPs) and around new technologies.

What your business needs is a way to get genuinely legitimate customers through the necessary checks quickly and easily, while ensuring compliance and stopping fraud at the gates.

1. Verify the identity of your customer

The first and most important step is to implement an identity verification (IDV) process that ensures your remote customers are who they say they are. The simplest IDV processes involve an automated ID check, but advanced verification demanded in some jurisdictions could involve a fully recorded and manually reviewed session including selfies and a photo with their selected ID. Sophisticated IDV software can also analyse the device and network used for a verification session to make sure you know everything you need to, including if your customer is even real.

What your business needs is a way to get genuinely legitimate customers through the necessary checks quickly and easily, while ensuring compliance and stopping fraud at the gates.

2. Screen global sanctions and watchlists

Once you’ve confirmed your potential customer is who they say they are, the next step is to ensure they are on the right side of the law. That means screening individuals and businesses against global watchlists for fraudsters, terrorists and other bad actors. The best third-party AML screening providers use thousands of sources to provide comprehensive global coverage of sanctions, PEPs, and watchlists.

Fast decisions

A 98% check automation rate gets customers through in about 6 seconds.

Simple experience

Real-time end user feedback and fewer steps gets 95% of users through on the first try.

Document coverage

An unmatched 13.5K+, and growing, government-issued IDs are covered.

More conversions

Up to 30% more customer conversions with superior accuracy and user experience.

Better fraud detection

Veriff’s data-driven fraud detection is consistent, auditable, and reliably detects fraudulent forms of identification.

Scalability embedded

Veriff’s POA can grow with your company’s needs and keep up with times of increased user demand.

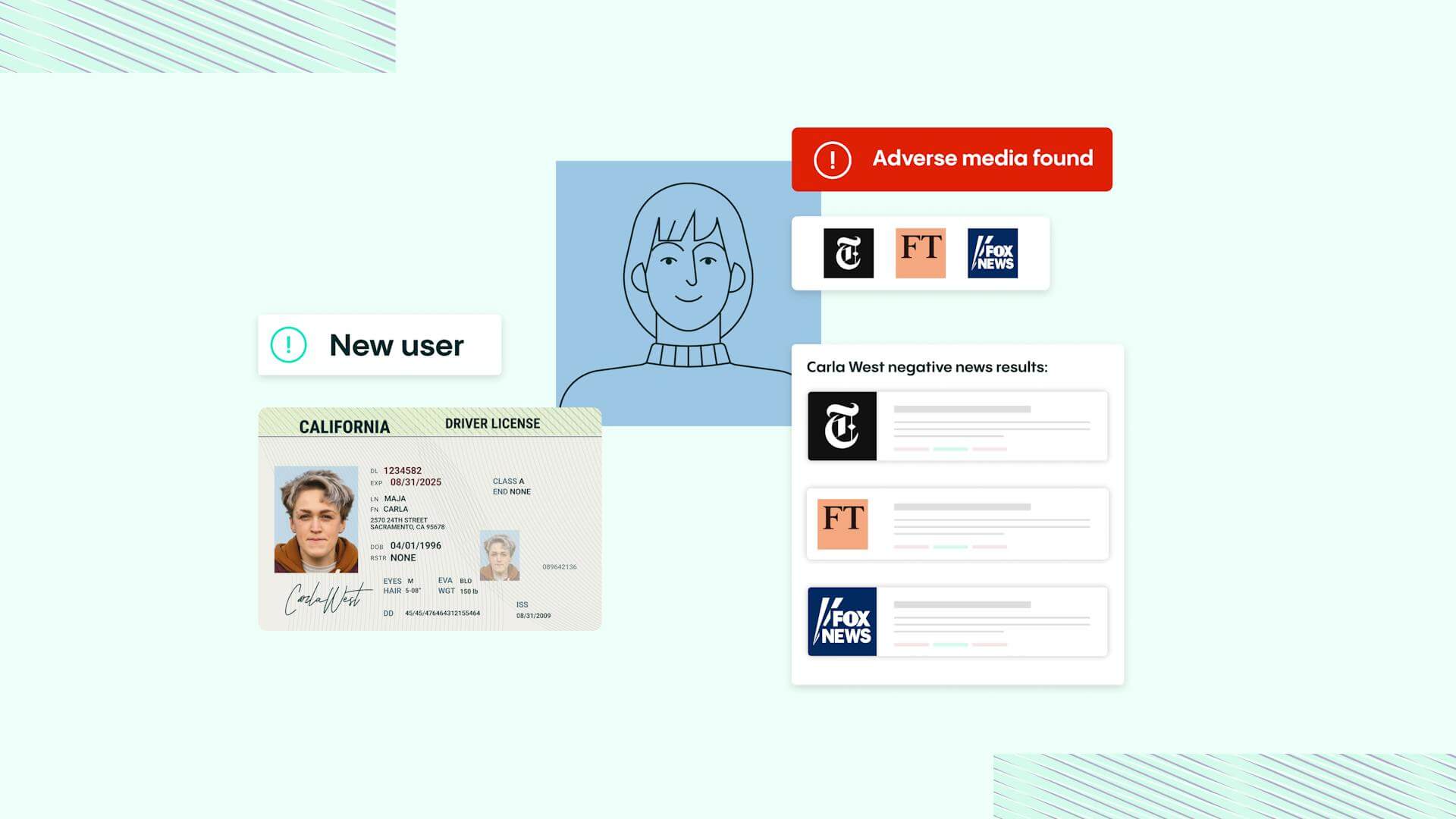

3. Check for negative news

As part of your AML approach, you also want to have in place a process to identify negative news concerning predicate offences that may be relevant and present a risk. These include everything from illegal arms sales, terrorism and drug trafficking, to cybercrime, counterfeiting and market manipulation. Again, the best AML providers will offer a relevant service as part of their offering.

4. Ensure ongoing monitoring

It’s important to keep in mind that the AML process doesn’t end once a customer has been onboarded. Political and regulatory environments are constantly changing, so you need to be constantly alert to new issues. A good third-party provider will continuously monitor global watchlists and adverse media for changes that may create risk, providing you with real-time data and updates on emergent threats. They can even provide direct notifications if your existing customers match with persons newly added to watchlists.

Employing AML screening that incorporates automated IDV, PEP and sanctions checks, adverse and media screening, and ongoing monitoring reduces risk for your business on both sides of the equation. With the right solution, you can demonstrate to regulators that you take financial crime seriously and ensure compliance, while converting more customers through a more seamless onboarding process. You can also scale more easily, because working with an experienced provider with a flexible approach will give you protection against spikes in volume of customers onboarding.

Get more details

Discover more about how IDV is powering Neobank growth and customer acquisition