How ID Verification can be the Game Changer

With millions of people around the world unbanked, could Veriff be a part of a wider solution to help our economy reach people who've never had access before?

Chris Hooper

A free-flowing economy needs money to be readily available. Consumers with access to their money have more choices, more financial freedom and are more likely to make impulse or advertising-inspired purchases. Currently, over 1.2 million Britons and 24.2 million US citizens are unbanked, meaning they don’t have access to bank accounts, debit cards and other everyday financial products. For Britons alone, the personal cost is an estimated £485 each per year, translating into a significant shortfall at the tills.

The problem of the unbanked

If there is one thing that defines this issue, it’s how long it has in fact been a problem. There are certain demographics that, for one reason or another, could not be easily screened for current account services, and were for many years unable to get a bank account.

Traditionally, the unemployed, those with bad credit history, or people with no fixed abode suffered from a serious lack of options when it came to banking services and financial products.

Banks blamed the inability to screen certain people for accounts, so brought in the solution of basic bank accounts. With the advent of the electronic debit systems such as Visa Electron and Switch’s Solo, these basic bank accounts soon came with debit cards and basic deposit and withdrawal functionality.

That said, there is still an issue. Migrants, homeless people, and ex-offenders, both in the UK and US, still have issues when trying to access basic banking. As mentioned above, there are still 25.2 million unbanked citizens within the UK and US at the date of the most recent reports.

What can banks and governments do to help?

Due to the strict laws and regulations surrounding banking in many countries, traditional banks are very much at the mercy of local laws within the countries they’re operating. But there are steps financial institutions can take to meet governments halfway.

Having a secure and trustworthy verification process can mitigate much of the red tape handed down from the government. And banks seem to be taking identity verification (IDV) seriously, and are less likely to fall foul of heavy sanctions and restrictions from nervous, cautious, or heavy-handed governments.

Governments, however, are not without their own obligations. This is unfortunately where British and US banks suffer, as these countries are yet to implement compulsory ID cards that have been seen around Europe to significantly reduce fraud and identity theft.

Therefore, the issuing of official documents for those entering these countries as migrants, or even for citizens that have neither travelled or passed a driving test, is seen as an essential step. There are currently many people in the UK alone who do not have any ID for this very reason.

Banks must also step up and work flexibly with governments on accepting documents that might be issued. Better communication between databases would also see an increase in the number of individuals that could be trusted, based upon information collected about income, assets, and employment status.

Thriving economies need people who can spend their money easily

The individual cost of being unbanked has already been touched upon above, but what about that of the wider economy? It has been long accepted that consumers are more likely to spend if the journey from inception to purchase is made as smooth as possible. Retailers and service providers can only take this so far, and always with the assumption that the customer themselves has instant access to their funds.

The negative effect on a country’s economy from having that journey interrupted is often significant, and the risks normally associated with granting access to financial products to higher-risk individuals are potentially far less serious. Coupled with the availability of trusted third-party IDV providers like Veriff, the resulting damage to the economy from lack of access to cash far outweighs any potential risk burden for banks and governments alike.

How to mitigate the risks and introduce a standard

The greatest challenge to new and existing financial service providers is the lack of a universal, international system for ID verification. Especially in countries without a standard national ID system, verifying customers and assessing risks have required a great deal of resources and manpower.

The UK and US often rely on crude methods such as providing proof of address using old bank statements or utility bills, or even accepting testimonials from family doctors, teachers, librarians (yes, really) and other ‘pillars of the community’ as ID verification for those without a passport or driving licence – all far from secure and based on tired stereotypes of who can and can’t be trusted. Functional fifty years ago maybe, but not appropriate for a post-millennial world, and certainly not suitable for cryptocurrencies.

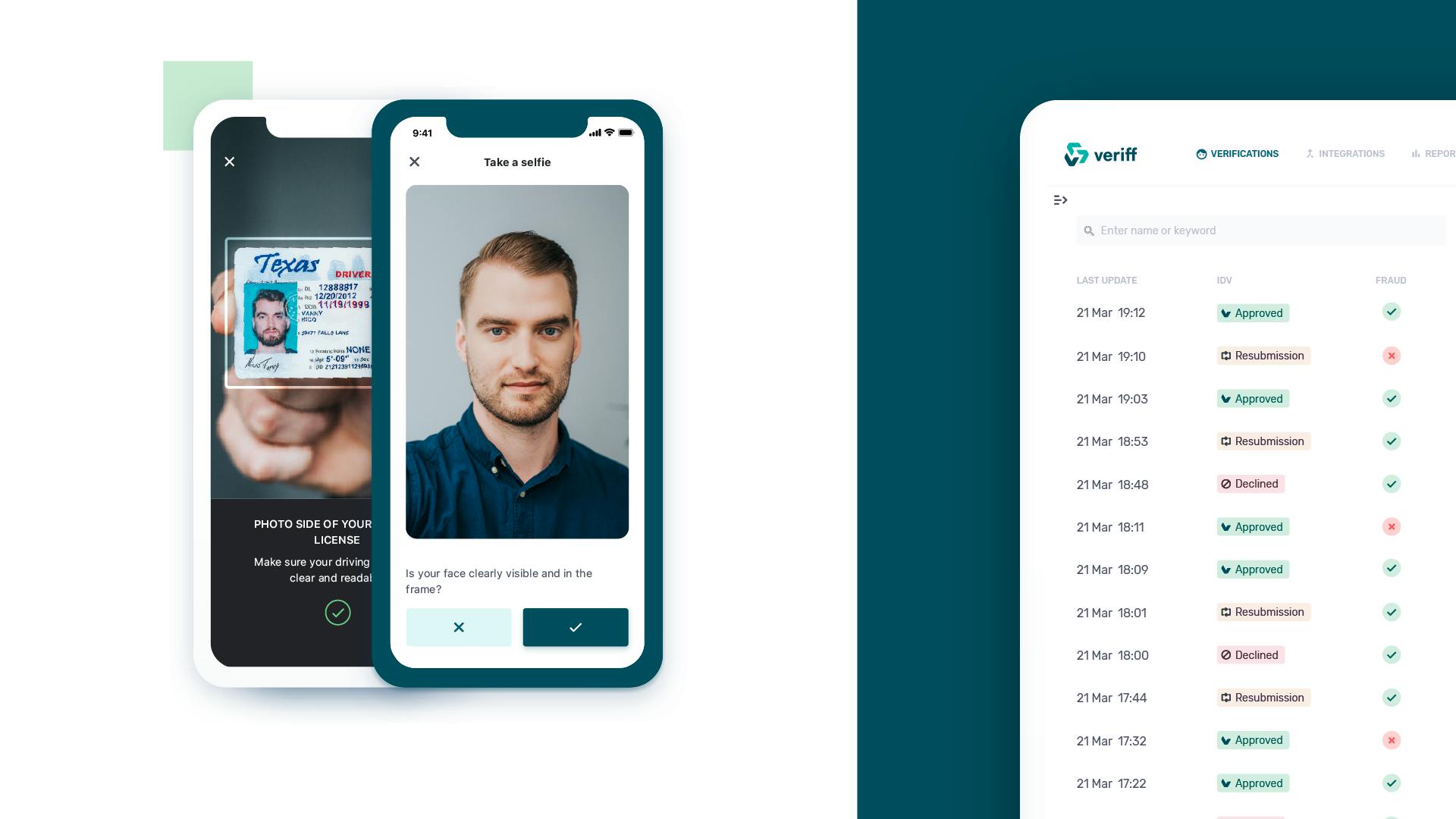

Using a tool such as Veriff creates a level playing field, and allows for a secure, trusted, and tamper-free identity check. Even without the digital security that our checks include, using a third-party has always been safer. Our 95% first-time success rate, with checks taking from as little as a few seconds through an integrated end-to-end verification service, provides the game-changing universal IDV banks have been after some time.

Compatible with today’s banks, and crypto-ready

Having struggled to be seen as trustworthy, cryptocurrencies have gained some bad press. Lack of consumer understanding is usually the cause, but the anonymous nature of crypto hasn’t helped it disassociate with the murky world of fraud and money laundering.

Companies involved with crypto are now acutely aware of the need to verify and screen their customers to be taken seriously in terms of security and trustworthiness. Licences and compliance for companies incorporating crypto into their consumer products demands a diligent approach to KYC (Know Your Customer) practices; licences are easily lost should these standards slip.

Traditional and crypto-based businesses entering the financial services markets today know the importance of rapid growth and scaling. Tough competition and an increasingly crowded market put extra pressure to onboard clients swiftly and with minimum effort. Veriff’s solution helps with conversion rates, allows for simplicity, and gets your product or service in front of as many clients as possible.

Naturally, a more efficient onboarding process may bring its own challenges. Higher volumes of sign-ups will inevitably see more cases of attempted fraud. Using a universal, trusted verification system will weed-out the fraudulent applications behind the scenes, whilst allowing valuable, trustworthy new sign-ups to pass through the process without delay – especially well-suited to crypto-based businesses.