KYC Article

Financial Conduct Authority finds challenger banks are not doing enough to fight financial crime

The Financial Conduct Authority (FCA) has warned challenger banks that they need to stop cutting corners when attempting to combat financial crime. Currently, the regulator believes that processes that allow customers to set up accounts quickly and easily are stopping challenger banks from conducting appropriate checks.

The Financial Conduct Authority (FCA) has warned challenger banks that they need to stop cutting corners when attempting to combat financial crime. Currently, the regulator believes that processes that allow customers to set up accounts quickly and easily are stopping challenger banks from conducting appropriate checks.

Challenger banks fail to put risk assessment processes in place

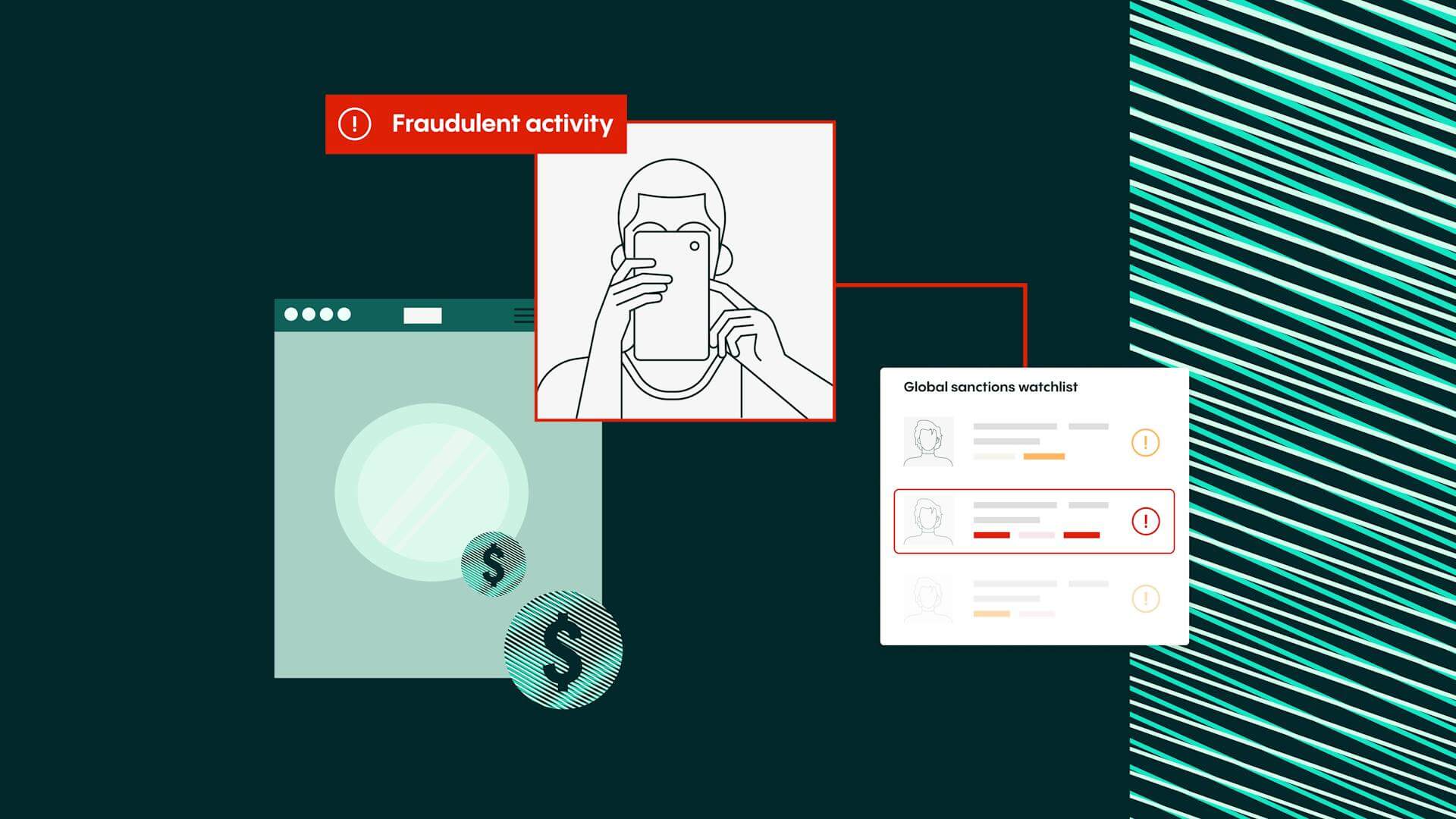

Following a study, the regulator found that many challenger banks do not currently have proper customer risk assessment processes in place. Such assessments are key ways of ensuring that a bank knows who its customers are and can manage the risks of money laundering. This is a legal requirement for companies that are covered by the UK’s money laundering regulations.

The FCA said that “without a customer risk assessment, a firm can’t ensure that due diligence measures and ongoing monitoring are effective and proportionate to the risks posed by its individual customers.”

Financial crime systems must be enhanced

The regulator added that although challenger banks are an important part of the UK’s retail banking offering, there must not be a trade-off between quick and easy account opening and robust financial crime controls. Due to this, challenger banks must enhance their financial crime systems in order to prevent harm.

As part of their study, the FCA found that challenger banks were not correctly identifying high-risk customers, who were then onboarded and remained customers for years before being spotted. It’s the view of the FCA that many of these customers should not have been onboarded in the first place and that better controls and risk assessments would have identified these people sooner.

On top of this, the FCA says that although challenger banks are sending an increasing number of reports to regulators about suspicious customer transactions, the quality of these reports can be poor. For example, some reports simply list transactions without explaining why they are suspicious.

Ensure compliance with Veriff

With the help of our AML and KYC compliance solutions, your financial institution can ensure compliance with KYC regulations at every step of the customer journey.

With the help of our solution, you can deploy our identity verification platform alongside PEP and sanctions checks and adverse media screening. This way, you can accurately assess the potential AML risk exposure of each customer. Plus, our powerful solution also allows you to monitor each customer on an ongoing basis. You’ll even be notified if something changes with your existing or previously onboarded customers.

Want to learn more about how Veriff can help you? Talk to us today.