Blog Post

What is due diligence in finance?

When carrying out due diligence, a financial institution must determine whether they should perform customer due diligence (CDD) or enhanced due diligence (EDD). This is because FATF guidance suggests that companies should adopt a risk-based approach to due diligence that reflects the specific level of risk that each individual customer presents.

In the world of finance, due diligence refers to the process of establishing and verifying the identity of a customer.

By verifying the identity of their customers and gaining an understanding of the nature of the business in which they are involved, a financial institution can begin to understand the level of money laundering risk posed by each customer.

Customer due diligence is a key part of the know your customer (KYC) process. All Financial Action Task Force (FATF) member states must implement due diligence processes as part of the fight against money laundering and terrorist financing.

Types of due diligence needed in financial sectors

Due diligence is required in a number of different circumstances. Financial institutions should follow the due diligence process when:

- Establishing a new business relationship

- An occasional transaction involves an amount of money that exceeds a regulatory threshold or involves a high-risk foreign country

- There’s a suspicion of money laundering

- A customer has provided unreliable or inadequate information

Plus, customer due diligence should also continue on an ongoing basis as part of the business-customer relationship. This is because the process ensures that the customer’s transactions and behaviors are consistent with their established risk profile.

When carrying out due diligence, a financial institution must determine whether they should perform customer due diligence (CDD) or enhanced due diligence (EDD). This is because FATF guidance suggests that companies should adopt a risk-based approach to due diligence that reflects the specific level of risk that each individual customer presents.

Customer due diligence (CDD)

As part of the customer due diligence process, a financial institution must establish the identity and business activities of their new potential customer.

Once they have identified the customer, the financial institution must then categorize that customer’s risk level. When the risk level has been established, the company will then determine whether more intensive enhanced due diligence measures are required.

Enhanced due diligence (EDD)

High-risk customers are subjected to more onerous EDD checks. Examples of these customers include politically exposed persons (PEPs) and customers who are the target of economic sanctions.

As part of the EDD process, these customers will be asked to provide further identification materials and establish the source of their funds or wealth. Then, the financial institution will apply closer scrutiny to the nature of the business relationship or purpose of a transaction, and implement rigorous ongoing monitoring procedures.

By only employing EDD processes when needed, companies can balance their compliance obligations with their budget and preserve customer experiences.

Why financial businesses must have due diligence checks in place

The due diligence process plays a big part in countering the growing threat of money laundering. It also prevents crimes like terrorist financing, human and drug trafficking, and fraud. However, there are a great number of reasons why financial institutions must have due diligence processes in place.

For example, if a financial institution fails to put proper due diligence processes in place it faces huge regulatory consequences. Since 2009, regulators have levied approximately $32 billion in AML-related fines globally and, in 2020 alone, FinCEN fined banks in the United States a total of $11.11 billion.

On top of this, a failure to put adequate due diligence processes in place can also cause a huge amount of reputational damage. If money launderers are able to access your service, your customers and prospects will no longer trust your security systems.

What gets checked?

Performing a due diligence check involves identifying your customers, verifying that they are who they say they are, and accurately analyzing the level of risk they pose.

Due to this, in practical terms, the due diligence process involves obtaining a number of pieces of information from the customer, including their:

- Full name

- Residential address

- Date of birth

The financial institution will then ask the customer to produce an identity document that can verify this information, plus a live selfie that can be matched to the photo on their government-issued ID. The information provided by the customer can then be checked against third-party databases, such as watchlists and sanctions lists.

Depending on the nature of the relationship, the institution may also ask for information regarding the activities the customer is engaged in, the markets they operate in, and the other entities a customer does business with.

With this in mind, let’s take a look at exactly how due diligence checks are performed.

How to perform a due diligence check

At the start of a due diligence check, a customer is usually asked to fill in an online form. At this stage of the process, they’ll be asked to provide the basic identifying information outlined above.

Next, the customer will be asked to provide a photo of a government-issued identity document, such as a driving license, passport, or ID card. This is usually captured with their smartphone or a webcam, depending on whether they’re using a phone or a computer.

Following this, the customer will be asked to take a selfie. The financial institution can then check that this selfie has been taken live, hasn’t been manipulated, and matches the picture on the identity document. In doing so, they can verify that the person providing the information is also the person pictured on the identity document and the owner of that identity.

At this stage of the process, the financial institution can also check the information the customer has provided against a variety of third-party databases. In doing so, they can verify that the customer exists and is legitimate. They may also check for a number of fraud signals, such as the IP address used and the speed at which the online form was completed by the user.

Now the user’s identity has been established and verified, they will be screened against government-issued watchlists and politically exposed persons (PEP) lists. Based on the results of all these checks, the user will then be assigned to a risk pool. Those who are flagged as high risk will be subjected to EDD checks.

At this stage, the user can be onboarded. Following this, they must be monitored on an ongoing basis to ensure their behaviors and transactions are consistent with their risk profile.

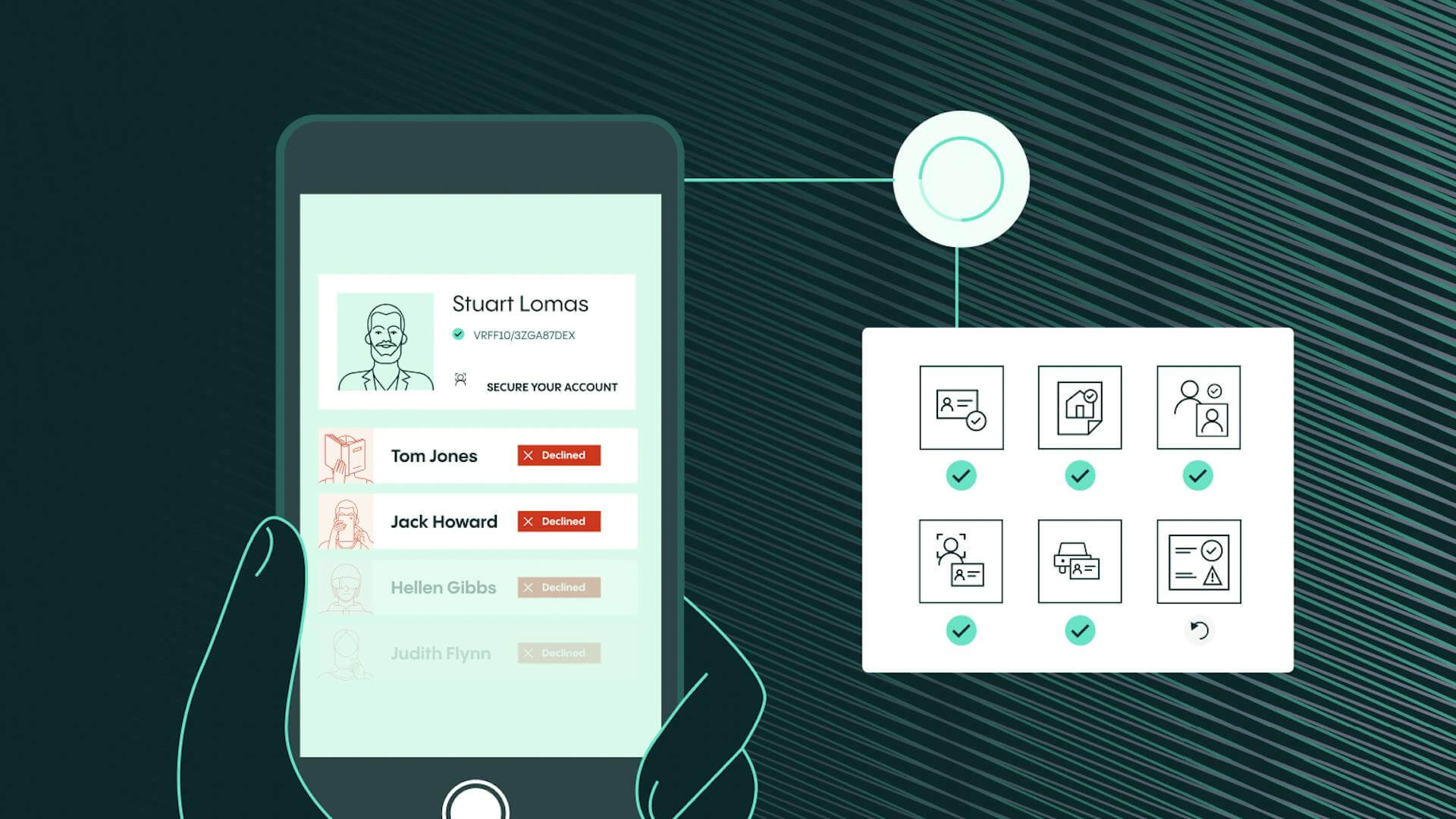

How can Veriff help?

As you can see from the above, if your company cannot create efficiencies and automate part of the customer due diligence process, then the process can become incredibly long and complicated. This can cause customers to turn away from the process and lead to your conversion rates plummeting.

Thankfully, here at Veriff, we’ve developed a range of solutions that can be used as part of your customer due diligence process. In particular, our AML and KYC compliance solution can help you show regulators that you take financial crime and compliance seriously, while also making it easy for honest customers to access your services.

The solution starts with identity verification. With accurate and automated decision-making, it stops bad actors in their tracks and provides honest customers with a decision in only six seconds. Assisted image capture helps guide the user through the process, and biometric authentication is 99.9% accurate.

In addition, the solution also screens global sanctions and politically exposed persons lists, which are updated in real time. As a result, as well as ensuring regulatory compliance, it also bolsters confidence in your due diligence and KYC process. Following this, Veriff also screens for negative information and news to help your business accurately assess the potential anti-money laundering risk exposure of each customer.

Then, once onboarded, our solution provides ongoing monitoring. Political and regulatory environments change very quickly, but our ongoing monitoring of PEP watchlists, global sanctions lists, and adverse media helps you stay on top of your customers. You’ll also get notified if anything changes.

Speak with the online verification experts at Veriff

If you’re interested in learning more about how our solutions can help your business improve its due diligence process, then speak with the online verification experts at Veriff today.

Simply provide us with some basic pieces of information about you and your business and we’ll present you with a personalized demo that shows exactly how we can help you. Get in touch today to arrange a demo for a time that suits you.