Blog Post

5 points for KYC best practice

Although the KYC process is mandatory, it can also be incredibly expensive if your processes are ineffective and bloated. This is particularly the case when you include factors such as manual hours, staff hires, and the price of any compliance tools. Discover how to overcome the barriers that prevent KYC best practice.

Every year, banks and financial institutions spend billions of dollars implementing processes that help them meet their AML and KYC requirements. However, in spite of spending huge sums of money, many of these financial institutions purely implement KYC processes as a ‘box ticking exercise’.

But, when implemented in this fashion, these KYC processes can be both costly and ineffective. They can also annoy customers and lead to poor retention rates. On top of this, financial institutions that don’t use effective KYC processes also miss out on the opportunity to leverage customer intelligence and improve the customer experience.

With this in mind, here we’ll outline five forms of KYC best practice that can boost the effectiveness and efficiency of your KYC processes.

Improve data quality

If you improve the quality of data collection and apply the right analytics during the KYC process, you will receive a number of benefits. After all, if you improve data quality, you can tap into deep customer intelligence and insights. This will help you improve your risk management and the customer experience.

On top of this, by improving the quality and the accuracy of the data you collect, you can also improve your ability to service customers, lower your costs, and boost revenue.

According to a recent survey, data quality problems currently account for up to 26% of operational costs. This is because many companies are dealing with non-standardized data formats, duplicate data, and incomplete data.

To overcome the problems associated with poor data quality, a number of top organizations are working towards creating a single, global customer view that effectively utilizes real-time data. By investing in the right technology and analytical capabilities, these businesses can achieve sustainable growth.

Plus, these organizations are now putting disciplined data management practices in place that leverage automatic and dynamic data feeds from external and internal sources. Using this data, these organizations can conduct advanced analytics processes that provide them with a competitive advantage when it comes to KYC.

Incorporate automation

Leading on from the above, the best financial institutions are also harnessing the power of automation as a form of KYC best practice. This is because automation can help businesses reduce their costs, shorten the onboarding process, and improve accuracy.

By automating the KYC process with the help of a piece of software, you can ensure end-to-end anti-money laundering compliance, as well as compliance with KYC protocols.

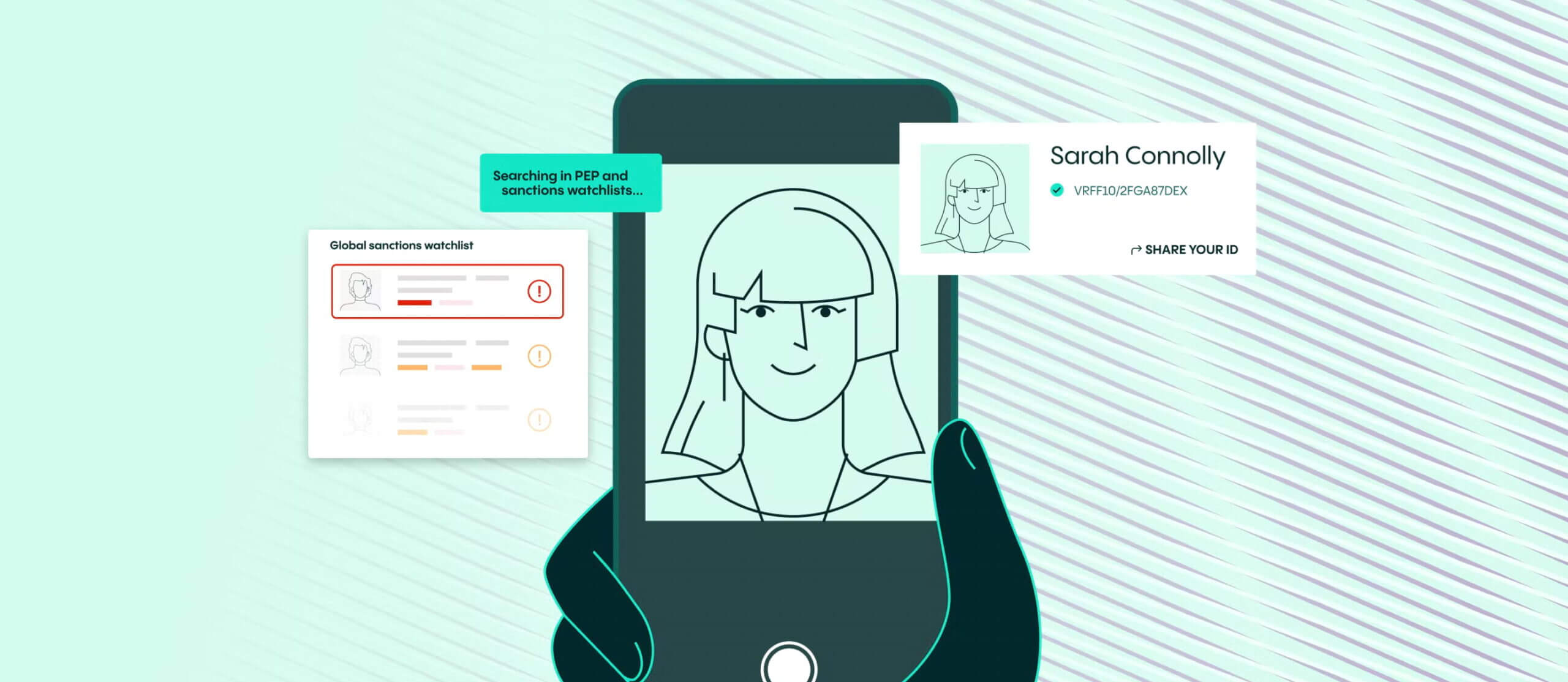

With our AML and KYC compliance solution, you can verify the identity of your customers, screen them against PEP and sanctions watchlists, check for adverse media and information, and monitor them on an ongoing basis.

Our automated and accurate identity verification process can verify the identity of a user in only six seconds. Plus, the solution can also check for liveness and the Assisted Image Capture functionality helps guide a user through the process, so you can boost conversions.

Reduce false positives

If your customer’s name matches the name of someone on a politically exposed persons (PEP) watchlist, or they attempt to make a legitimate number of business withdrawals in a business day but accidentally cross a threshold, then they’ll create a false positive AML alert.

All AML alerts need to be scrutinized by your AML compliance team. As a result, if your processes generate a high number of false positives, then you could be wasting huge sums of both time and money. On top of this, if you freeze the account of a customer who has triggered a false positive, then the inconvenience may cause them to switch providers.

Although it’s near impossible to eliminate false positives entirely, there are steps you can take to reduce the number of false positives you generate. For example, you can:

- Restructure your data; particularly names

- Make sure data is both relevant and accurate

- Review your processes regularly and continually adapt them

- Employ the use of smart technologies, such as artificial intelligence and machine learning

Improve customer outreach

Customer outreach is a critical step in a KYC process. It refers to the information a business requires from its customers in order for the customer due diligence (CDD) process to take place.

The more onerous your customer outreach process is, the lower your conversion rate will be. This is because some customers are unwilling to part with sensitive information. Meanwhile, others will become increasingly frustrated when they’re asked to provide information they’ve already supplied, or if the process is unnecessarily slow.

For this reason, you should review your customer outreach process. Although you need to make sure you capture enough information to remain compliant with customer due diligence requirements, you should take all possible steps to make sure your customer outreach process is frictionless and quick.

Look to reduce costs

Finally, it’s impossible to talk about KYC best practice without discussing cost. Although the KYC process is mandatory, it can also be incredibly expensive if your processes are ineffective and bloated. This is particularly the case when you include factors such as manual hours, staff hires, and the price of any compliance tools. This is before we even consider the sunken cost of customers abandoning their application due to KYC friction.

Thankfully, when you follow all the advice we’ve outlined above, you’ll find it easy to reduce your KYC costs. This is because you’ll make the process far less manual, better organized, and user friendly.

Plus, if we return to the point regarding automation, not only can you save staff time, but you can also find an automated solution that reduces costs and suits your budget. For example, our essential verifications start from as little as $1.49.

How Veriff supports with KYC compliance

Here at Veriff, our solutions support KYC compliance. With the help of our AML and KYC compliance solution, you can fight financial crime, deploy KYC best practices, and show regulators that you take financial crime and compliance seriously.

To discover more about how we can help improve your KYC processes, talk to us today.