ON THIS PAGE

August 27, 2025

Onboarding Article

KYC Address Verification: The critical shield against fraud

In a world that prizes both instant access to financial services and ironclad security, KYC address verification has become an essential frontline defense. Gone are the days when verifying a customer’s address was simply a regulatory hurdle. Today, KYC Address Verification acts as a multi-layered safeguard against identity theft, financial crime, and regulatory risk. For financial institutions, the sophistication and accuracy of their verification systems are vital to prevent fraud, maintain operational efficiency, and uphold customer trust throughout their verification processes.

KYC Address Verification plays a vital supporting role within Know Your Customer (KYC) and Customer Due Diligence (CDD) frameworks, complementing identity verification at its core. By verifying a customer’s identity and ensuring submitted documents are accepted as proof of address, organizations can comply with anti-money laundering (AML) regulations and the recommendations set forth by the Financial Action Task Force (FATF). This, in turn, creates seamless onboarding experiences that support legitimate users while keeping criminals at bay.

The high stakes of modern customer onboarding

Modern customer onboarding sits at a critical intersection: Today’s customers expect rapid approvals and a frictionless journey, but financial institutions have to balance these demands with increasingly rigorous regulatory requirements and evolving fraud risks.

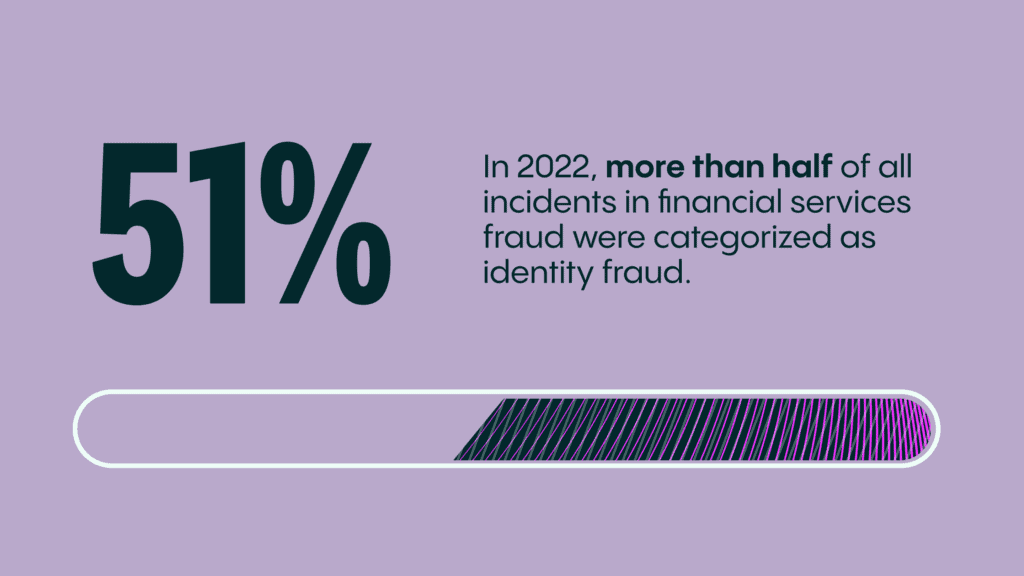

The numbers emphasize what’s at stake. According to Veriff’s Fraud Report 2025 and Future of Finance Report:

- Online fraud rose by 21% year-on-year in 2024, following a 20% surge the previous year.

- 5% of all verification attempts in 2024 were fraudulent, highlighting the sophistication of threats.

- 13% of fraud decision-makers revealed fraud costs up to 20% of their revenue.

These figures underscore the need for reliable proof of address verification, strong verification processes, and modern verification systems. Without robust controls to verify a customer’s identity and authenticate proof of address documents, organizations risk significant financial exposure and reputational harm. By mastering KYC address verification, businesses don’t just stay compliant—they build trust and earn customer loyalty in an increasingly competitive market.

Why is KYC Address Verification essential?

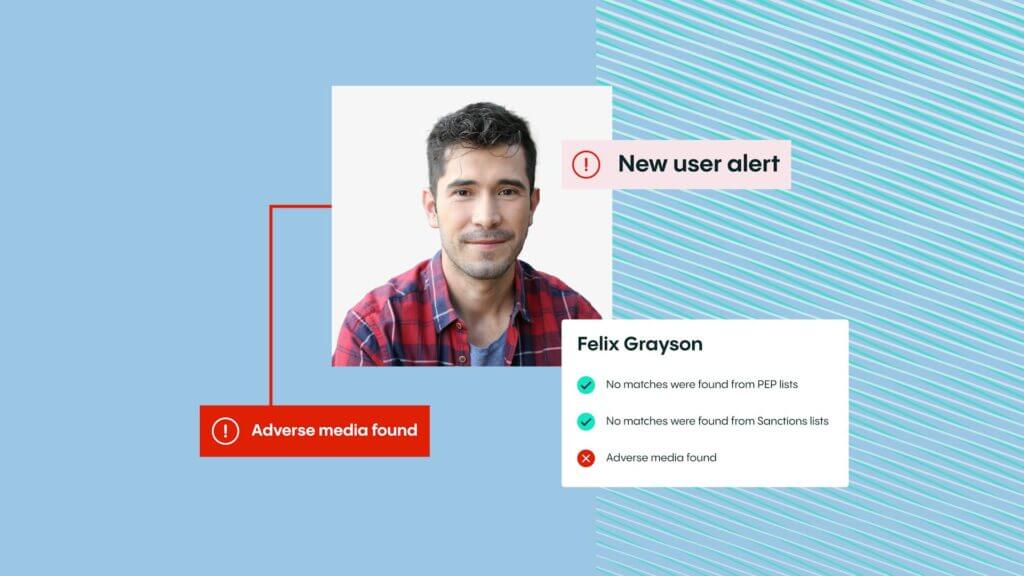

1. Fraud prevention

With schemes like identity theft and synthetic fraud on the rise, financial institutions rely on layered verification systems to prevent fraud. Criminals attempt to breach KYC protocols by presenting fake government-issued IDs or manipulated utility bills, or bank statements. Robust proof of address verification employs advanced document forensics, monitors for repeated or suspicious addresses, and validates data against trusted sources.

These multi-step verification processes are crucial not only for stopping fraudulent onboarding attempts but also for detecting emerging fraud risks that might slip through simpler systems. When financial institutions enforce high standards for what is accepted as proof of address and use technology to back it up, they create significant barriers for malicious actors.

2. Regulatory compliance

Adhering to anti-money laundering (AML) laws and FATF recommendations isn’t optional—it’s essential for doing business. Successful customer due diligence (CDD) means collecting, validating, and securely storing both proof of identity and valid proof of address. Documents like bank statements, lease agreements, or utility bills must satisfy criteria for timeliness and authenticity, and the entire process must be audit-ready for regulators.

Failure to meet these standards can result in steep fines, reputational loss, and increased scrutiny from regulators. With stringent verification systems and clear procedures around proof of address verification, organizations protect against these risks while safeguarding their own operational continuity.

3. Seamless customer onboarding

In digital banking and fintech, onboarding speed can make or break the customer experience. Outdated or cumbersome verification systems, especially ones that cause unnecessary manual review, drive away prospective users. By automating document collection, verification, and cross-checking of utility bills or bank statements, organizations can instantly verify a customer’s address, reduce drop-off rates, and foster positive first impressions.

Best-in-class KYC Address Verification solutions offer customers step-by-step guidance, flag incomplete submissions, and deliver rapid approvals for acceptable proofs of address. This seamless process positions financial institutions as trustworthy, efficient, and customer-centric.

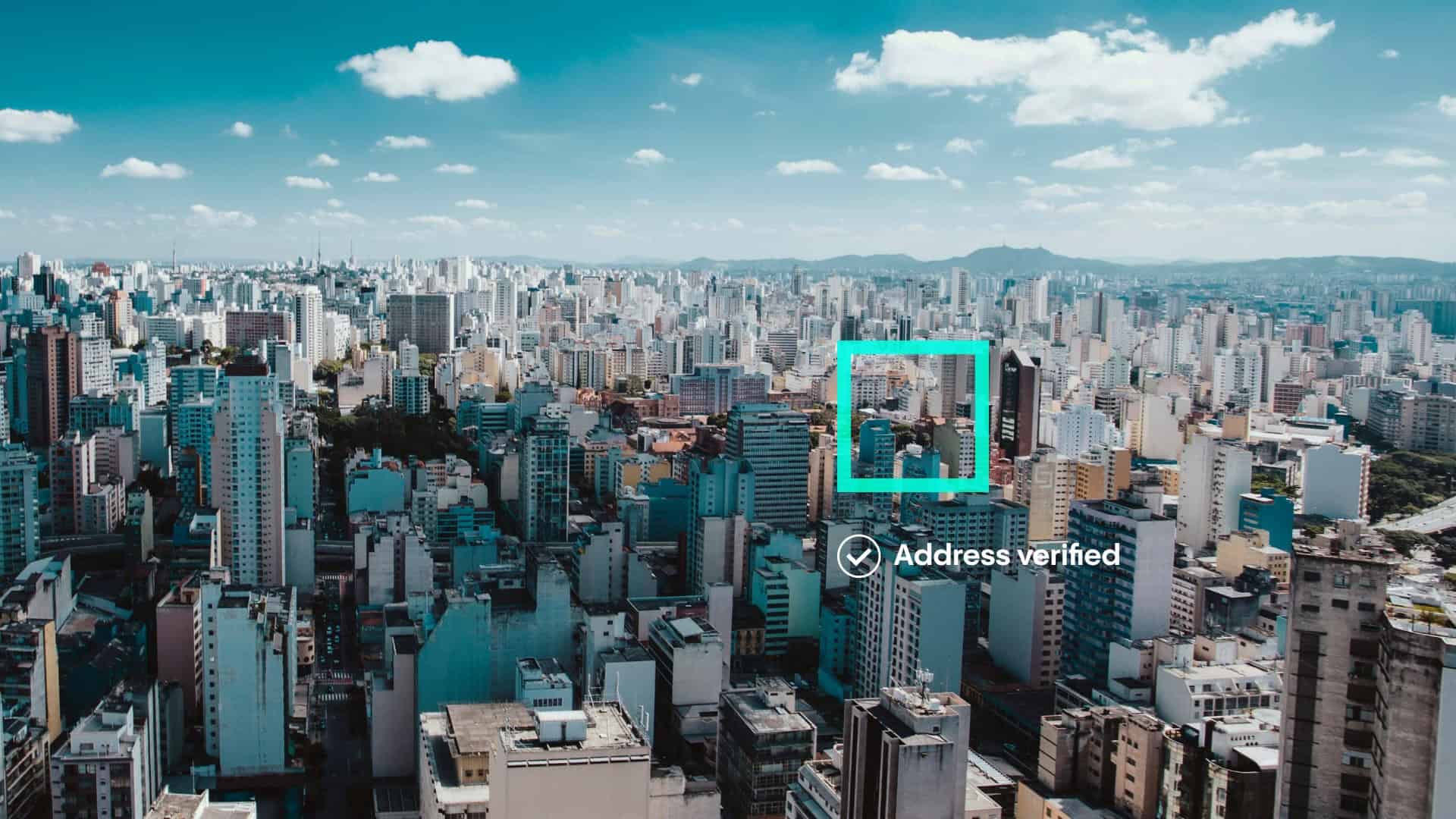

How modern address verification works

Today’s KYC address verification combines technology, regulatory know-how, and risk management by following a clear workflow:

- Document collection: Customers upload crisp images of accepted proof of address documents: utility bills, bank statements, lease agreements, or government correspondence.

- Data extraction: OCR and AI tools capture the address details and analyze the document for signs of digital manipulation or forgery.

- Authenticity and security checks: The verification system reviews document layouts, fonts, and embedded security markers and compares them with known templates.

- Database cross-verification: The extracted address is matched against third-party data sources (postal records, government databases) to verify legitimacy and association with the customer’s identity.

- Decision and escalation: Clean cases are approved, while outliers and anomalies are flagged for further manual review by compliance teams.

These advanced verification processes allow financial services providers to adapt to new fraud tactics, scale across borders, and maintain regulatory alignment.

The LHV bank case study: Building trust with digital verification

A tangible example of KYC address verification’s importance comes from LHV Bank, a digital-first financial institution in the UK’s fiercely competitive market. To launch quickly without compromising security, LHV sought a partner who could deliver smooth customer onboarding and the highest standards of fraud defense.

Working with Veriff, LHV integrated biometric checks and advanced verification systems for both proof of identity and address. Customers could upload government-issued IDs and documents accepted as proof of address, like utility bills or bank statements, during onboarding. Veriff’s rigorous verification processes helped prevent fraud, ensuring only those with valid proofs of address could access LHV’s innovative financial services. As Kris Brewster, Director of Retail Banking, explained, “Veriff challenged our ideas about what was possible, responded to our pace, and kept our defenses strong without impacting the user experience.” LHV’s approach exemplifies how coordinated verification systems and strong KYC Address Verification underpin safe, agile growth for modern financial institutions.

Implementation best practices for KYC Address Verification

To succeed in today’s climate, organizations must be strategic and agile with their verification processes:

- Define accepted documents: State which documents: utility bills, bank statements, lease agreements, are considered accepted as proof of address in your regulatory context.

- Keep up with changing regulation: Regularly align your policies and practices with current anti-money laundering (AML) and Financial Action Task Force (FATF) guidance.

- Leverage automated verification systems: Use AI-powered verification systems and machine learning to minimize manual review, boost detection rates, and scale globally.

- Routinely analyze outcomes: Track verification rates, fraud cases, manual escalation frequency, and update processes to optimize results.

- Prepare for global and edge cases: Enable international customers, recent movers, or those without utility bills to provide alternative proof of address documents, like government-issued IDs with address, or lease agreements.

The future of KYC Address Verification

As technology advances, the importance of secure, scalable verification will only grow. Artificial intelligence will further enhance document analysis, fraud pattern recognition, and access to real-time data sources. Financial institutions will be able to automate even more of the customer due diligence workflow while complying with evolving AML rules and FATF standards.

Digital onboarding will keep raising the bar for both speed and security. Successful organizations will invest in robust proof of address verification, seamlessly integrate it with proof of identity measures, and use verification systems that support continuous improvement. This approach not only prevents fraud and guards against identity theft, but also meets rising customer expectations and regulatory scrutiny.