A Guide to Anti-Money Laundering (AML) Compliance

Staying two steps ahead of criminals demands a fast-evolving regulatory environment. The new AMLD5 directive will impact governments as well as companies, and here is everything you need to know to stay compliant in 2020.

Mario Alfaro

On June 19, 2018, the European Union kickstarted its new anti-money laundering directive, AMLD5. The new directive builds on the points made in the AMLD4, with changes designed to strengthen anti-money laundering efforts and combat the financing of terrorism. To help you navigate through the new directive, the following guide includes the highlights and tips for staying compliant in 2020.

This guide starts with an overview anti-money laundering laws, followed by the details you need to know to stay AMLD5 compliant in chapters below:

- An overview of anti-money laundering and the AMLD5

- The 6 key AMLD5 guidelines explained

- The industries affected by AMLD5 guidelines

- The importance of being AML compliant

- How to stay AML compliant in 2020

1. What is anti-money laundering?

Understanding anti-money laundering starts with examining money laundering as a crime.

Money laundering is a criminal process of converting or transferring assets with the intent to hide their origins. This typically happens when the assets come from illegal activity. The process of money laundering disguises these illicit origins, making them appear to be legal.

This is where the phrase “washing” or “laundering” money comes in, as the money laundering process involves cycling assets through various businesses and holdings until the source is difficult to trace.

As a general term, anti-money laundering refers to the entire system of rules, procedures, laws, and regulations that are designed to prevent money laundering crimes. Most developed countries have laws or a set of regulations in place against money laundering.

In the case of the European Union, its parliament published directives that member states must adopt into their legislation to address this problem, the latest being the AMLD5.

2. The 6 key AMLD5 guidelines explained

January 20, 2020, the deadline set by the EU Commission for each member of the European Union to implement the new directive, is just around the corner. This means that governments, and companies, need to act fast to stay compliant.

The AMLD5 includes a series of new guidelines aimed to strengthen anti-money laundering regulations and protect honest people. In a nutshell, what this directive focuses on is bringing more transparency to institutions in the European Union. Below are the most important items addressed in the new directive.

2.1. Ultimate beneficial ownership (UBO)

This guideline gives the general public access to information regarding the Ultimate Beneficial Ownership (UBO) of companies based in the European Union. This register will be accessible to all competent authorities (without any restrictions) and will help prevent the misuse of legal entities to launder money or finance terrorism.

2.2. Politically exposed persons (PEPs)

All EU member states will be obliged to create a list of public offices and their functions at a national level, which will be cataloged as politically exposed persons (PEP).

The idea behind this is that the member states of the European Union should name the positions that they consider PEPs, but it will not be necessary to specify the names of the people in each role. This is a challenge for each company that wants to comply with the new law because to do so requires them to monitor any changes in these positions.

2.3. High-risk third countries

Countries that have precarious anti-money laundering regulations, which are categorized as high-risk countries, will have stricter due diligence demands. This guideline will standardize processes across financial institutions and other entities obliged in relation to enhanced due diligence (EDD).

Eliminating these weak links will significantly reduce the entry of money from illegal sources in high-risk third countries into the European Union.

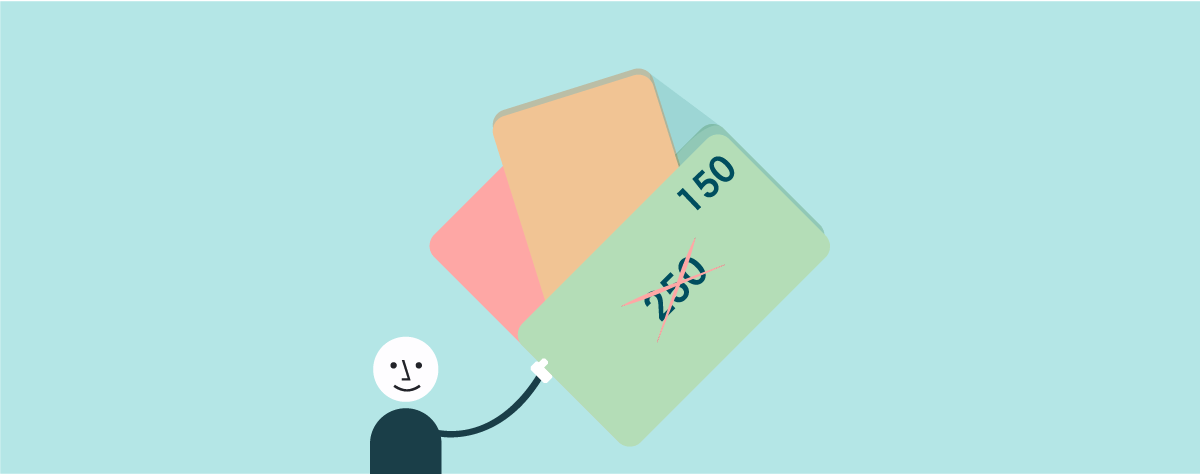

2.4. Prepaid cards

The threshold for identifying holders of prepaid cards will be lowered from €250 to €150. Online transactions with prepaid cards will also be limited to a maximum of €50. Member states intending to further restrict this measure will also be able to do so at their own discretion.

2.5. Crypto markets

The anti-money laundering regime will be extended to the cryptocurrency sector to prevent any type of risk from virtual currencies. In the future, all electronic platforms that include cryptocurrency exchanges will be covered by the AMLD5. In the past, these types of platforms were unregulated, making them vulnerable to money laundering crimes.

People who operate in this virtual space will have to have a broader understanding of AML laws. Something to consider is whether the regulation of virtual currencies undermines the premise of anonymity and decentralization that made it flourish in the first place.

2.6. Monitoring Financial Intelligence Units (FIUs)

Under the AMLD5, more power will be given to Financial Intelligence Units (FIUs), who facilitate cooperation and information exchange between authorities. The member states of the European Union must establish national registries for banks so that they are able to identify all accounts of any person by the corresponding FIU.

3. The industries affected by AMLD5 guidelines

When anti-money laundering regulations come to mind, they are usually associated with financial institutions, specifically banks, as the key institutions that need to comply. Today, the reality is very different.

Since the emergence of industries like cryptocurrencies and fintech solutions, AML regulations apply to a much broader spectrum, including:

- Financial institutions

- Credit institutions

- Auditors, external accountants, and tax advisors

- Trusts and company service providers

- Legal professionals, including notaries

- People trading in goods where cash payments are made in amounts of €10,000 or more

- Estate agents

- Providers of virtual currencies

Art dealers and virtual currencies need to be extra careful

As mentioned earlier, cryptocurrencies and crypto wallets will be affected by the new AML directive. This means that the industry will be forced to meet the same rigorous standards as financial institutions, including regulations like customer due diligence, transaction monitoring, and suspicious activity reports.

The world of crypto is not the only new industry to fall under the AMLD5’s jurisdiction. Agencies and art dealers will also need to start verifying their customers’ identities, as well as maintain an audit trail when transactions are greater than €10,000.

4. The importance of being AML5 compliant

In light of recent events like the terrorist attacks in Brussels and Paris and the liberation of the Panama Papers, the inadequacy of anti-money laundering systems in Europe is difficult to ignore.

The United Nations Office on Drugs and Crime (UNODC) estimates that around 5% of the global GDP is laundered annually, in this case, we are talking about $800 billion to $2 trillion that is subjected to the laundry cycle. Taking into account that this money is used to fund illicit businesses, AML directives are essential for combating and preventing the financing of crime.

While understanding the guidelines is the first step, it is also necessary to distinguish between complying as a member of the European Union or as a private institution conducting business.

AML non-compliance fines for private institutions

For private institutions and businesses, failing to comply with the new regulations will be met with high fines and even criminal prosecutions. During the year 2019, the Financial Authority of the United Kingdom (FCA) imposed fines for over $1 billion, while in the rest of Europe, banks paid over $16 billion in fines between 2012 and 2018.

5. How to stay AML compliant in 2020

Today we live in a digital society that comes with many benefits and risks. Cybersecurity challenges like online fraud evolve quickly, and anti-money laundering regulations are only one way to ensure that money does not end up in the hands of criminals.

The only way to stay compliant with the anti-money laundering regulations is to keep an eye out for new directives that the European Council plans on issuing.

Beyond staying up to date on AML regulations, another way to be compliant is to invest in a reputable KYC service provider who helps to comply with the AML regulations. KYC providers that employ artificial intelligence and machine learning to keep businesses compliant can reduce the risk of human error, as well as ease the process for your in-house team.

When looking for an KYC solution, it is important to keep the following tips in mind:

- Look for a service provider that is willing to adapt their service based on your specific needs rather than a service that takes a one-size-fits-all approach. Many KYC providers do not take into account the complexity of their business, which is why a customizable provider that is willing to adapt and cooperate with you is much better than a generic solution.

- The KYC solution you are looking for must include AML or consumer due diligence (CDD) features that are robust enough to comply with the new regulations. These functions can either be fully outsourced or shared with the company’s program depending on your needs.

- It is necessary to have revision control, including the re-evaluation of anti-money laundering programs. We live in a society that is rapidly modernizing, meaning that regulations adapt quickly, too. That’s why it is necessary for the KYC service you choose to have a scheduled update scheme to deal with these updates.

Get the AML compliance you need with Veriff

As a KYC service and fraud prevention partner, Veriff helps companies enforce AMLD5 guidelines by making sure your customers are who they say they are.

In addition to KYC compliance, Veriff provides PEP and Sanctions Checks, device, browser, and network fingerprinting, and other anti-fraud tools to keep you compliant in today’s fast-paced regulatory environment.

For more details on Veriff’s fraud-prevention features, check out our product page. You can also sign up for a free 30-day trial of our self-service platform, Veriff Station, giving you the same fraud prevention tools used by Enterprise clients with flexible pricing plans designed to grow with you.